The Centre’s decision to raise ₹13,000 crore via Offer for Sale in three public sector banks is less about disinvestment optics and more about fiscal arithmetic. With GST buoyancy slipping below 1.0 and refund delays taxing exporters, the government’s revenue strategy is shifting toward asset monetisation. OFS in state‑run banks signals two simultaneous pressures: the need to shore up non‑tax receipts to meet deficit targets, and the political calculus of reducing state ownership without triggering market instability. In this Vishleshan, we decode why OFS is not just a fundraising tool but a stress test of India’s fiscal balance — weighing capital market depth, banking sector resilience, and the limits of consensus in public sector reform.

Businesses embrace GST, but seek more reforms: Deloitte survey

Context: Nine years into GST, the Deloitte India survey of 1,096 C-suite executives delivers what looks like a report card: 99% positive or neutral experience, robust ₹1.94 trillion May collections, and near-universal adoption. The article frames this as a maturity story — “GST 2.0” has arrived and businesses are ready for the next phase. This Vishleshan agrees with the direction but challenges the framing: the 99% satisfaction figure conceals a structural divide between large enterprises (who designed their operations around GST) and MSMEs (who are still managing cash flow crises caused by it). The survey’s “positive or neutral” binary hides the real story — compliance is accepted, but the working capital damage from refund delays and ITC disputes remains unresolved and is growing more acute as collections scale up.

Link to the Article: Mint

Background

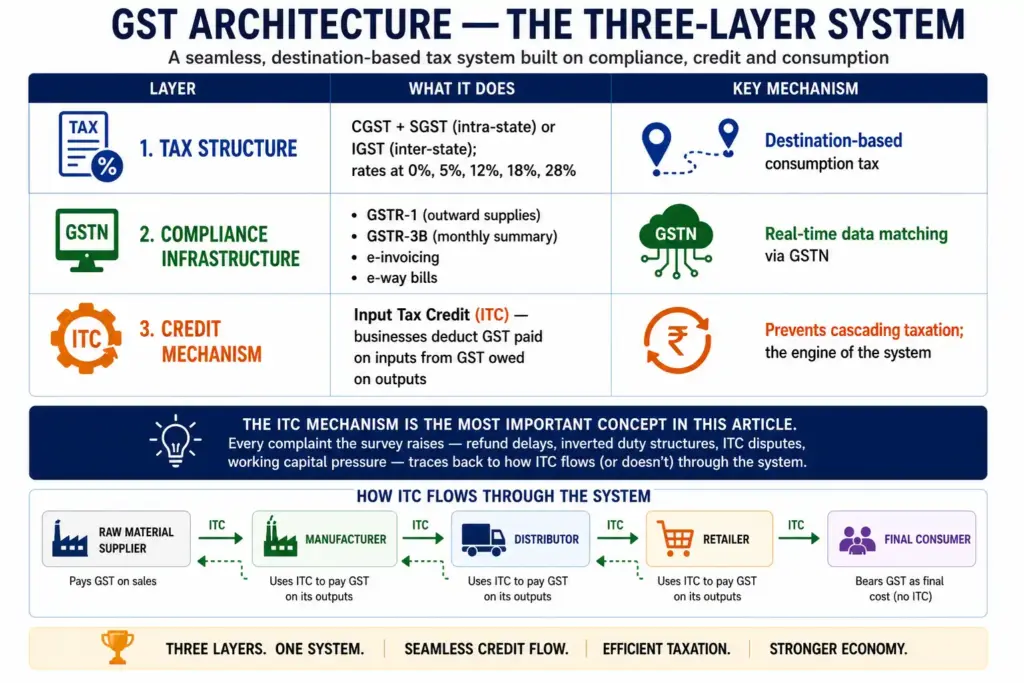

Input Tax Credit (ITC) — How It Works and Where It Breaks

How it works (when functioning correctly):

- A manufacturer buys raw materials, pays 18% GST on inputs

- Sells finished goods, collects 12% GST on output

- Net GST liability = output tax collected minus input tax paid

- If input tax > output tax → refund due from government

| Failure Mode | How It Manifests | Who Is Hurt Most |

| Inverted duty structure | GST on inputs is higher than GST on outputs → chronic refund accumulation | Textile, pharma, fertiliser manufacturers |

| Refund delays | Government processes refunds in 30–90+ days despite legal 60-day limit; interest at only 6% p.a. after delay — so low that delayed payment is financially rational for government | Exporters, MSMEs, working capital-intensive businesses |

| ITC mismatch disputes | Buyer’s ITC claim blocked if supplier hasn’t filed/ filed incorrectly | All businesses dependent on small/unregistered suppliers |

| Blocked credit | Certain categories (construction, motor vehicles, hospitality) explicitly denied ITC | Real estate, hospitality, infrastructure sectors |

| RCM (Reverse Charge Mechanism) | Recipient pays GST on behalf of supplier — but can only claim ITC later, not at point of payment | Cash flow gap for all RCM-covered transactions |

The MSME vs. Large Enterprise Divide — The Survey’s Hidden Variable

The survey covers MSMEs, large companies, and very large enterprises but presents aggregate results. The one MSME-specific data point the article gives is critical:

Quarterly return filing satisfaction: 12% (2023) → 67% (2026) — a 55 percentage point jump

This jump is almost entirely explained by the QRMP scheme (Quarterly Return Monthly Payment), introduced in January 2021, which allowed small taxpayers (turnover < ₹5 crore) to file returns quarterly while paying tax monthly. Before QRMP, small businesses filed monthly returns — an enormous compliance burden for proprietors with no dedicated tax staff. The 67% figure means 1 in 3 MSMEs still does not find quarterly filing adequate — a large residual dissatisfaction for what should be the most straightforward reform.

Inverted Duty Structure — The Most Underexplained Term in the Article

What it is: When the GST rate on inputs is higher than the GST rate on outputs, a manufacturer perpetually accumulates ITC it cannot use — because its output tax liability is always smaller than its input tax paid.

Classic example — fertiliser sector (rates current as of 2026):

- Inputs (packing material, chemicals, services) taxed at 12–18% GST

- Fertiliser output taxed at 5% GST

- Every tonne of fertiliser produced generates a refund obligation from the government

- At scale, this creates a structural working capital drain — businesses are effectively pre-financing the government’s refund obligation

Why 69% of respondents want the refund formula expanded to cover all input taxes: Currently the refund formula for inverted duty structures is deliberately restrictive — it covers only input goods, not input services. A manufacturer paying 18% GST on freight, warehousing, and professional services cannot include those in the inverted duty refund claim. Expanding the formula to include all inputs would eliminate the largest remaining source of ITC accumulation for affected sectors.

Decoding the Article: Analysis

1. The 99% Satisfaction Figure Is a Binary Trap That Conceals the Real Story

The headline number is striking: “99% reporting a positive or neutral experience.” The article presents this as evidence that GST has been broadly accepted. It is — but “positive or neutral” is a binary that makes the figure almost meaningless as a policy signal.

Consider the alternative: would any C-suite executive at a company operating in India for 9 years tell a Deloitte surveyor that GST has been a “negative” experience? The reputational and regulatory exposure of that answer — especially for a named, senior executive — is enormous. The survey methodology itself creates selection bias toward positive responses. “Neutral” is the honest answer for anyone who has adapted to the system but still finds it costly; “positive” is the safe answer. “Negative” is career risk.

The actual story is in the demand numbers, not the satisfaction binary. 87% seek interpretational clarity. 67% flag working capital pressure. 69% want refund formula expansion. 61% demand uniform audits. If 99% are happy but 87% are seeking fundamental policy reform, the “happiness” is compliance acceptance, not system satisfaction. The article conflates the two. A more accurate headline: “Nine years in, businesses have adapted to GST but the structural costs — ITC disputes, refund delays, interpretational ambiguity — remain unresolved and are the dominant focus of the next reform phase.”

2. The Refund Delay Problem Is Not Just a Liquidity Issue. It Is a Structural Tax on Exporters That Directly Affects India’s Export Competitiveness.

- The article frames refund delays as a “working capital” issue — businesses want faster refunds to manage cash flow. This framing is correct but significantly understates the economic cost.

- Indian exporters are zero-rated under GST — they pay GST on inputs but receive a full refund, since exports are not taxed. This means every rupee of GST refund delay is effectively a tax on Indian exports — the exporter has pre-financed the government and is waiting for repayment.

- On a ₹1 crore GST refund delayed by 60 days at a working capital borrowing rate of 12% per annum, the hidden financing cost is approximately ₹2 lakh — or 0.2% of the export value. The government’s statutory interest rate for delayed refunds is 6% per annum — so low that delayed payment is financially rational for the exchequer: it borrows from exporters at 6% in a 12% market. Multiplied across India’s ~$450 billion goods export base, even a 1% effective delay tax represents ~₹6,750 crore in annual hidden export cost.

- This is not an abstraction. India’s export growth has consistently underperformed peers (Vietnam, Bangladesh, Mexico) in labour-intensive manufactures — sectors dominated by MSMEs and small exporters who are most vulnerable to refund delays.

- The GST Council has introduced multiple refund acceleration measures (IGST refund automation, single-authority disbursement) since 2017 — but the Deloitte survey shows that faster refunds remain a top demand in 2026, nine years in. The article does not name the export competitiveness cost of refund delays — which is the most important macroeconomic implication of this data point.

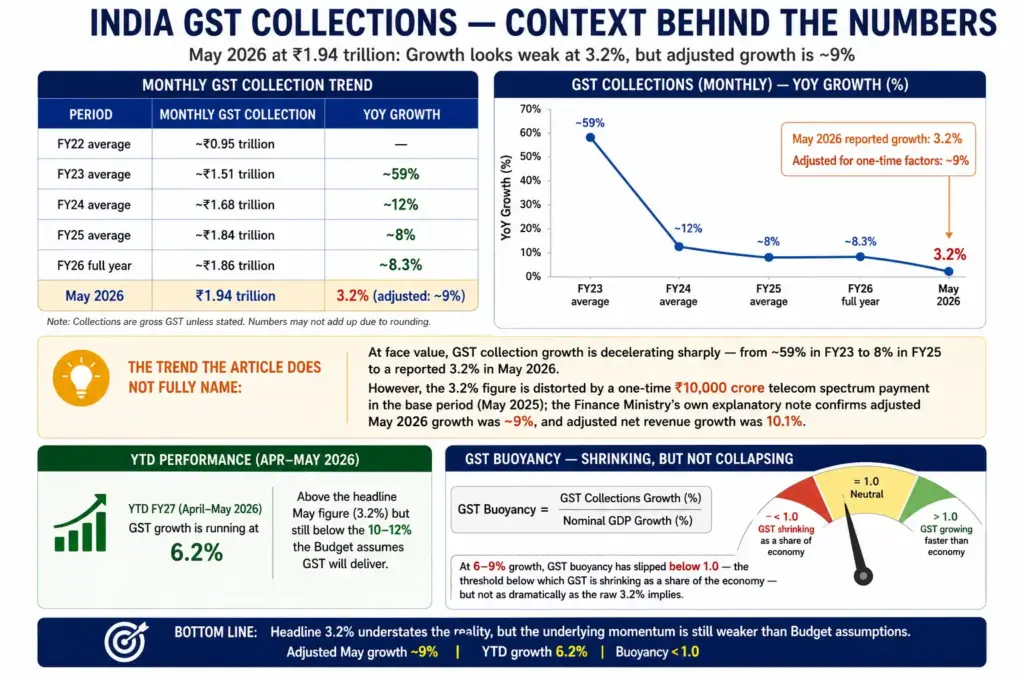

3. The Collection Growth Deceleration Is Real, Even After Stripping Out the Base Effect

The article cites ₹1.94 trillion in May 2026 GST collections, up 3.2% year-on-year, as evidence that “collections continue to be robust.” The Finance Ministry’s own clarification note flags that adjusted for a one-time ₹10,000 crore telecom spectrum payment in the May 2025 base, growth was ~9%.

The adjusted 9% is the honest number — and it still tells a concerning story. India’s nominal GDP growth in FY27 is tracking at approximately 10–11% (6.6% real + ~4% inflation). At 9% adjusted growth, GST buoyancy has slipped below 1.0 — the threshold below which GST is shrinking as a share of the economy. The YTD FY27 pace (April–May 2026) is 6.2%, well below the 10–12% the Budget typically assumes.

Three structural factors drive this deceleration:

(a) the informal-to-formal migration effect — the large one-time compliance gain from bringing informal sector businesses into GST is largely exhausted after 9 years;

(b) rate rationalization has reduced the effective rate on many categories — the GST Council has cut rates more than it has raised them over the decade;

(c) the Iran-war-linked slowdown in consumption in energy and auto sectors, two of GST’s highest-revenue categories, is visible in recent data.

The government will need either a rate hike (politically difficult), new categories brought into GST (petroleum products remain outside), or a consumption recovery to restore double-digit collection growth.

Fine Print — What the Article Quietly Skipped

The AI integration demand (89%) is the survey’s most forward-looking finding — and the article buries it. Nearly 9 in 10 respondents support AI for tax data processing and reconciliation. This is not a vague preference — it reflects a specific pain point: the GST reconciliation process (matching purchase register data with supplier-filed returns across GSTR-1, GSTR-2A, and GSTR-3B) is currently a monthly manual exercise for finance teams at large companies, involving hundreds of thousands of line-item matches. AI-assisted reconciliation would eliminate this entirely. The GSTN has been piloting AI-based mismatch detection since 2024 — but the 89% demand figure suggests the rollout is far behind business expectations. This is the GST reform with the highest ROI for business productivity and the least policy controversy — and the article gives it one sentence.

The “interpretational clarity” demand (87%) is a polite way of saying tax litigation has become systemic — and the new tribunal risks being overwhelmed before it finds its feet. GST was supposed to reduce indirect tax disputes, which under the pre-GST regime had created a ₹15+ lakh crore backlog in courts and tribunals. The GST Appellate Tribunal (GSTAT) became operational only in February 2026 — nearly nine years after GST’s launch. An estimated 2 lakh appeals are expected to be filed before GSTAT by the June 30, 2026 deadline alone (the window for pre-April 2026 adverse orders), against a tribunal that has been hearing cases for less than five months and currently has benches operational only in Delhi, Cuttack, and Chennai. The dispute resolution infrastructure arrived nine years late — and may be overwhelmed from day one.

The BFSI sector’s GST position remains structurally unresolved — and the article does not name it. Banks and financial institutions operate under a fundamentally different GST architecture from the rest of the economy — financial services are partially exempt, partially taxable, and ITC eligibility for mixed-supply financial institutions is governed by complex apportionment rules. The survey notes BFSI favoured “automation and integrated digital infrastructure” — which is the sector-specific language for: our ITC apportionment calculations are too complex to do manually and too error-prone to do without automation. The BFSI GST issue is a separate structural problem from the inverted duty or refund delay issues affecting manufacturing — and grouping all sectors into one “GST 2.0” narrative obscures how different the reform priorities are by sector.

Petroleum products outside GST is the survey’s loudest silence. The biggest structural incompleteness in India’s GST architecture — that petrol, diesel, aviation turbine fuel, and natural gas remain outside the GST framework — does not appear anywhere in the article or, apparently, in the survey findings. Every supply chain optimization argument in the survey is incomplete without acknowledging that transport costs (the largest input cost for most manufacturing and logistics businesses) are taxed under a pre-GST framework — with no ITC available. A manufacturer paying GST on all inputs but non-creditable taxes on fuel is still operating a hybrid tax system. The Deloitte survey of 1,096 C-suite executives somehow does not surface this — which either means the survey did not ask, or the finding was omitted from the article. Either way, it is the most important structural gap in India’s GST architecture and its absence from a 9th anniversary review is notable.

Nine years in, GST has won the compliance battle — 99% of businesses operate within the system, the digital backbone is functional, and ₹1.94 trillion in monthly collections represent a genuine fiscal achievement. But winning compliance is not the same as winning efficiency. The working capital damage from refund delays, the litigation accumulation from interpretational gaps, the structural distortion from petroleum exclusion, and the decelerating collection growth rate all point to a system that has been optimized for revenue extraction but not yet for economic neutrality. GST 2.0’s central challenge is not technological — it is political: every reform the survey demands (rate rationalization, refund expansion, petroleum inclusion) requires the GST Council to give something up. Nine years of consensus-building created the system. The next nine years will test whether that consensus can absorb the reforms needed to complete it.

- Sign Up on Practicemock for Updated Current Affairs, Topic Tests and Mini Mocks

- Sign Up Here to Download Free Study Material

Free Mock Tests for the Upcoming Exams

- IBPS PO Free Mock Test

- RBI Grade B Free Mock Test

- IBPS SO Free Mock Test

- NABARD Grade A Free Mock Test

- SSC CGL Free Mock Test

- IBPS Clerk Free Mock Test

- IBPS RRB PO Free Mock Test

- IBPS RRB Clerk Free Mock Test

- RRB NTPC Free Mock Test

- SSC MTS Free Mock Test

- SSC Stenographer Free Mock Test

- GATE Mechanical Free Mock Test

- GATE Civil Free Mock Test

- RRB ALP Free Mock Test

- SSC CPO Free Mock Test

- AFCAT Free Mock Test

- SEBI Grade A Free Mock Test

- IFSCA Grade A Free Mock Test

- RRB JE Free Mock Test

- Free Banking Live Test

- Free SSC Live Test