India’s latest ₹13,000 crore Offer for Sale (OFS) across three public sector banks — Punjab & Sind Bank, UCO Bank, and Indian Overseas Bank — is being projected as both a fiscal success and a sign of deepening market discipline in state-owned banking. But beneath the headline lies a more technical reality: this is not capital infusion, but ownership reshuffling triggered by Minimum Public Shareholding (MPS) compliance pressures rather than bank balance sheet needs. The proceeds will flow to the Consolidated Fund of India, not strengthen the banks themselves, making this fundamentally a regulatory and revenue exercise rather than a recapitalisation event. In this Vishleshan, we unpack how MPS norms, PSB valuations, and disinvestment architecture are converging into a narrative that looks like reform — but functions primarily as compliance.

Centre to raise ₹13,000 cr via OFS in three state-run banks

Context: The government plans an 8–10% Offer for Sale (OFS) in Punjab & Sind Bank, UCO Bank, and Indian Overseas Bank (IOB) to raise ~₹13,000 crore — primarily to comply with SEBI’s Minimum Public Shareholding (MPS) norm of 25% before the September 2026 deadline. This comes on the back of PSBs reporting record profits (₹1.98 lakh crore net profit in FY26), GNPA ratios at historic lows (1.93%), and the government’s FY27 disinvestment target of ₹80,000 crore — which it expects to overshoot for the first time in the post-pandemic period.

Link to the Article: Mint

Background

| Instrument | Who Issues | Who Gets Proceeds | Capital Impact on Bank | Government Retains Control? |

| OFS (Offer for Sale) | Existing shareholder (Government) sells existing shares | Government (selling shareholder) | None — bank gets nothing | Yes — just reduces stake |

| QIP (Qualified Institutional Placement) | Bank issues fresh shares to institutional investors | Bank (fresh capital) | Strengthens capital base | Yes — dilution shared |

| FPO (Follow-on Public Offer) | Bank issues fresh shares to public | Bank | Strengthens capital base | Reduces proportionally |

| Strategic Disinvestment | Government sells controlling stake | Government | None directly | No — control transferred |

- Key implication: This OFS does not strengthen the capital base of Punjab & Sind Bank, UCO Bank, or IOB. The ₹13,000 crore goes to the Consolidated Fund of India — not to the banks. This is purely a compliance + revenue exercise, not a capitalisation exercise.

The MPS Norm — What It Is and Why PSBs Have Struggled

SEBI’s Minimum Public Shareholding (MPS) Norm:

- Regulation 38, LODR Regulations: Every listed company must maintain at least 25% public (non-promoter) shareholding

- Rationale: Enhances liquidity, market depth, price discovery, and corporate governance

- Deadline for PSBs: Extended multiple times — latest relaxation from penal action valid until September 2026

- Penalty for non-compliance: Fines + freezing of promoter shareholdings (which would freeze government’s voting rights in these banks — a serious governance consequence)

Current government shareholding vs. MPS requirement:

| Bank | Govt. Shareholding | Public Float | MPS Gap | Implied Dilution Needed |

| Punjab & Sind Bank | 93.85% | 6.15% | 18.85% | Must sell ~18.85% of total shares |

| UCO Bank | 92.44% | 7.56% | 17.44% | Must sell ~17.44% |

| IOB | 90.95% | 9.05% | 15.95% | Must sell ~15.95% |

- The planned 8–10% OFS in each bank partially addresses the MPS gap — it does not fully close it in a single transaction

- Further rounds of dilution will be required post this OFS to fully comply by the September deadline

PSB Health Dashboard — Why the Timing Is Favourable

| Metric | FY26 Level | Significance |

| GNPA ratio | 1.93% | Historic low — from 11.6% peak in FY18 |

| Net NPA ratio | 0.39% | Near-zero net stress |

| Slippage ratio | 0.7% | Very low fresh stress formation |

| Total recoveries | ₹86,971 crore | Includes write-off recoveries |

| Aggregate operating profit | ₹3.21 lakh crore | Record |

| Net profit | ₹1.98 lakh crore (+11.1% YoY) | 4th consecutive year of record profits |

| CRAR | 16.6% | Well above 11.5% regulatory minimum |

- The NPA clean-up story — driven by IBC (Insolvency and Bankruptcy Code), SARFAESI enforcement, NARCL (National Asset Reconstruction Company Ltd.), and sustained credit growth — is now largely complete for PSBs

- This is the strongest balance sheet position Indian PSBs have been in since nationalisation-era complacency peaked pre-2015

Key Concepts: DIPAM, InvITs, and the Methodology Shift

DIPAM (Department of Investment and Public Asset Management): Nodal agency for managing government’s equity investments in PSUs and executing disinvestment transactions

Infrastructure Investment Trusts (InvITs): SEBI-regulated vehicles that pool investor funds to invest in operating infrastructure assets (roads, power lines, pipelines). The government monetises completed National Highway and power transmission assets by transferring them to InvITs and selling units to investors — generating capital receipts without selling equity in the PSU itself

The methodology change (February 2024): By discontinuing a separate disinvestment target and clubbing disinvestment + asset monetisation under “Miscellaneous Capital Receipts,” the government:

- Made the target harder to miss (wider definition)

- Made the accountability framework opaque (can’t separately track privatisation vs. asset recycling)

- Effectively acknowledged that strategic disinvestment (actually transferring control) is politically unachievable in the near term

Decoding the Article: Analysis

1. This Is Not Primarily a Disinvestment Story. It Is a Governance Compliance Story Dressed as Revenue.

The article’s framing — government expects to overshoot its ₹80,000 crore disinvestment target — suggests this OFS is part of a proactive disinvestment agenda. The actual driver is more mundane: SEBI’s September 2026 MPS deadline

Without the MPS deadline, there is no particular urgency to sell PSB stakes right now. In fact, selling when PSB valuations are near record highs is good timing — but the government has never historically sold PSU stakes at optimal valuations proactively. It has sold when forced to by fiscal needs or, in this case, regulatory deadlines

The September 2026 MPS deadline creates an unusual alignment: regulatory compulsion + good PSB valuations + fiscal need all pointing in the same direction simultaneously. This is rare — and the article attributes the timing entirely to the favourable PSB health story when the regulatory gun-to-head is equally, if not more, determinative.

2. The OFS-QIP Choice Has a Hidden Implication for PSB Capital Adequacy Under Basel III

The aggregate PSB CRAR of 16.6% masks significant heterogeneity. SBI, Bank of Baroda, and Punjab National Bank pull the aggregate up. Among the three OFS banks:

| Bank | Estimated CRAR | vs. 11.5% minimum | Buffer |

| Punjab & Sind Bank | ~13.8% | +2.3% | Thin |

| UCO Bank | ~14.2% | +2.7% | Moderate |

| IOB | ~15.1% | +3.6% | Comfortable |

Punjab & Sind Bank’s 2.3% CRAR buffer above the regulatory floor is the thinnest in the PSB cohort — an OFS that mildly depresses its share price without adding capital narrows, not widens, its future equity-raising headroom. A depressed share price means any future QIP to shore up Tier 1 capital must issue more shares for the same rupee amount, diluting existing shareholders further and deterring institutional participation

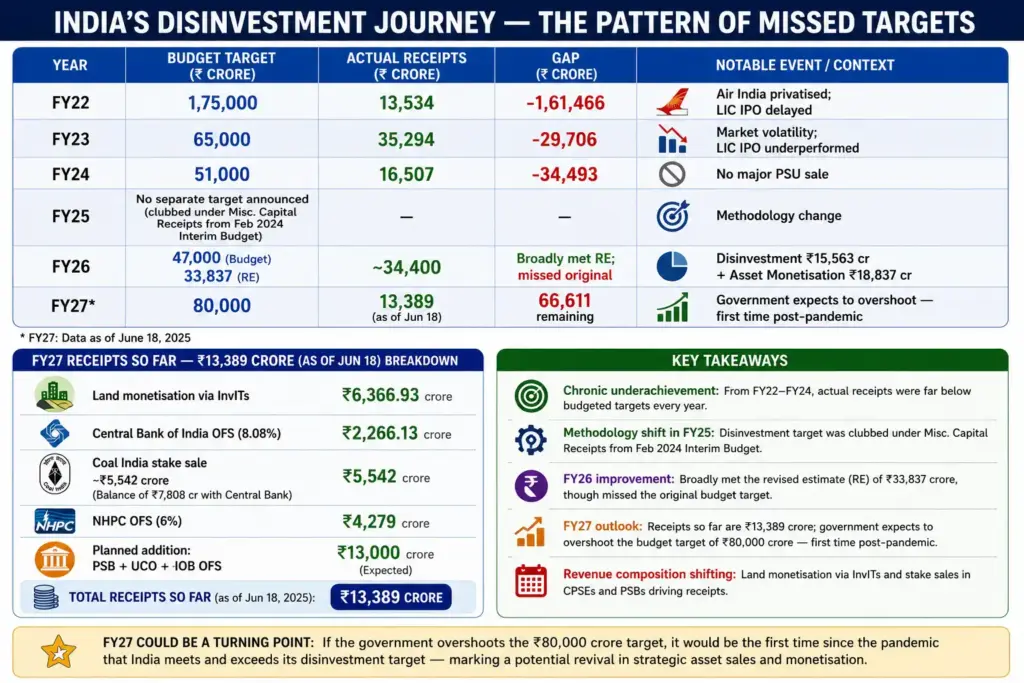

3. The ₹80,000 Crore Target Architecture Is More Fragile Than the “Expected Overshoot” Narrative Implies

- The article’s most bullish claim is that the government “expects to overshoot its ₹80,000 crore disinvestment target for FY27 — a first after consistently falling short in the post-pandemic period.” This needs aggressive interrogation

- What has been raised so far (₹13,389 crore) is entirely from:

- Asset monetisation via InvITs (land — not equity disinvestment)

- Small OFS transactions in PSBs (Central Bank, NHPC, Coal India)

- None of this involves strategic disinvestment (transfer of management control)

- What remains (₹66,611 crore): At the current pace of OFS-led bank dilutions (~₹2,000–4,000 crore per transaction), the government would need 15–30 more such transactions to meet the target. This is mathematically possible but operationally heroic — each OFS requires SEBI approval, floor price notification, investor appetite, and market conditions

- The “expected overshoot” narrative rests on two assumptions the article does not verify:

- Market conditions remain favourable through FY27 — the Iran war, monsoon performance, RBI rate trajectory, and global risk-off sentiment are all variables that could close the OFS window

- Asset monetisation via InvITs can be scaled up — the ₹6,367 crore InvIT component is land monetisation, which has its own pipeline constraints (how much government land is “monetisation-ready” and legally unencumbered?)

Fine Print

- The September deadline is probably soft, not hard. SEBI has extended the MPS deadline for PSBs multiple times since 2015. The penalty — freezing government’s voting rights in a bank — is so constitutionally awkward that it has never actually been imposed. The real pressure is reputational, not legal. The government is acting now because PSB valuations are favourable, not because SEBI will actually freeze sovereign shareholding.

- Punjab & Sind Bank is not the same as UCO or IOB. It is India’s smallest PSB, almost entirely Punjab-focused, heavily agri-linked, and has the thinnest capital cushion in the group. Institutional investors who are comfortable buying UCO or IOB may demand a steeper discount for Punjab & Sind Bank. The article treats all three as equivalent — they are not. Watch Punjab & Sind’s OFS subscription rate closely.

- The NPA clean-up didn’t happen by itself. The historic low GNPA of 1.93% is the output of three specific tools: IBC (forced resolution timelines), SARFAESI (collateral enforcement), and NARCL (National Asset Reconstruction Company — bought ~₹1 lakh crore of legacy stressed assets off bank books since 2021). Without naming these, the “historic low NPA” figure sounds like the banks just got lucky. They didn’t — policy architecture delivered it.

- ₹80,000 crore only looks achievable because the definition changed. Until February 2024, disinvestment meant selling PSU equity. Since then, it includes asset monetisation — land sales, InvIT receipts, toll proceeds. Of the ₹13,389 crore raised so far in FY27, nearly half came from land monetisation via InvITs, not equity sales. The “expected overshoot” is partly a target that was widened, not a disinvestment programme that was strengthened.

The real story of this OFS is not disinvestment ambition — it is the convergence of three forces that rarely align: a regulatory deadline the government cannot ignore, PSB balance sheets that are genuinely the strongest they have been in a generation, and a fiscal year in which the government has quietly redefined what counts as disinvestment success. If all three OFS transactions close before September, it will be declared a governance reform milestone. But the ₹13,000 crore will not strengthen a single bank, will not reduce the government’s control over a single institution, and will not move India any closer to the structural question it has deferred for two decades — whether state-owned banking at 93% government shareholding is compatible with a market-oriented financial system that can fund a $7 trillion economy.

- Sign Up on Practicemock for Updated Current Affairs, Topic Tests and Mini Mocks

- Sign Up Here to Download Free Study Material

Free Mock Tests for the Upcoming Exams

- IBPS PO Free Mock Test

- RBI Grade B Free Mock Test

- IBPS SO Free Mock Test

- NABARD Grade A Free Mock Test

- SSC CGL Free Mock Test

- IBPS Clerk Free Mock Test

- IBPS RRB PO Free Mock Test

- IBPS RRB Clerk Free Mock Test

- RRB NTPC Free Mock Test

- SSC MTS Free Mock Test

- SSC Stenographer Free Mock Test

- GATE Mechanical Free Mock Test

- GATE Civil Free Mock Test

- RRB ALP Free Mock Test

- SSC CPO Free Mock Test

- AFCAT Free Mock Test

- SEBI Grade A Free Mock Test

- IFSCA Grade A Free Mock Test

- RRB JE Free Mock Test

- Free Banking Live Test

- Free SSC Live Test