India’s virtual digital asset story is at a crossroads. What began as a taxation experiment with a 30% levy and 1% TDS has morphed into a regulatory vacuum where investors remain exposed. Offshore migration, systemic risks, and FATF non‑compliance now collide with the absence of a framework law. The $230 million hack and rising retail harm show that waiting for industry practice is no longer viable. In this Vishleshan, we decode why India must legislate first, define VDAs clearly, and build a “SEBI for crypto” to protect investors and financial stability.

Virtual digital assets: it’s time for India to get its regulatory act together—investors need protection

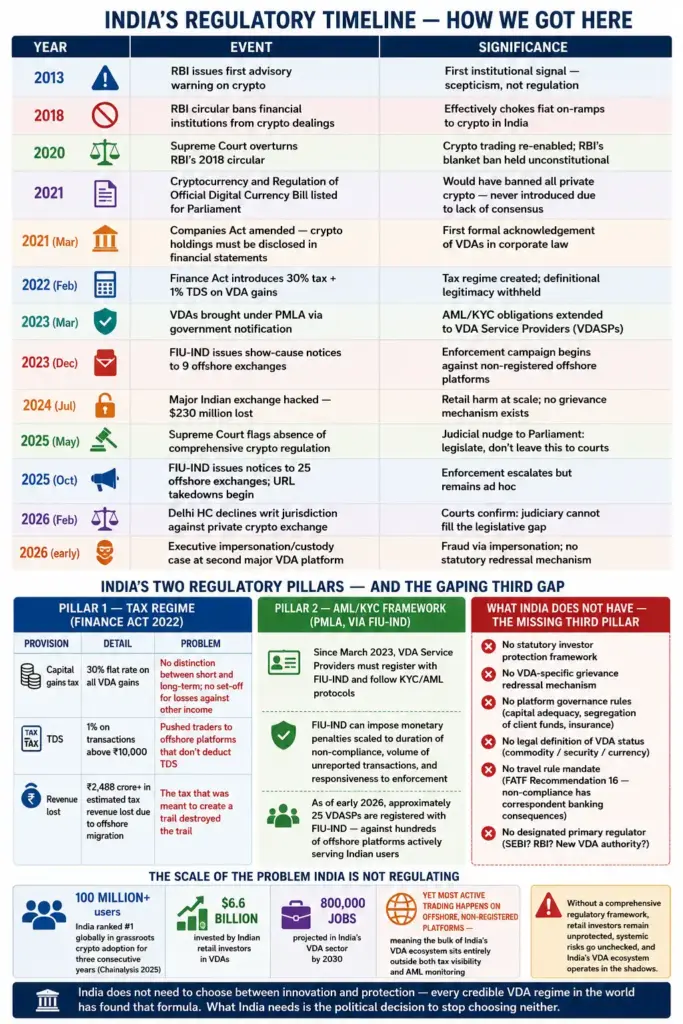

Context: India has over 100 million crypto users — ranked first globally in grassroots adoption for three consecutive years — yet its regulatory architecture consists of only two pillars: a punitive tax regime (30% flat tax + 1% TDS) and an AML/KYC framework. A $230 million exchange hack in 2024 left retail users with no statutory recourse; 2026 executive custody case exposed impersonation vulnerabilities with no grievance mechanism in sight. The article is essentially about why India’s ad hoc enforcement architecture — FIU-IND notices, URL takedowns, court-confirmed jurisdictional gaps — cannot substitute for a dedicated legislative framework, and what the building blocks of that framework must be.

Link to the Article: Mint

Background: India’s Current VDA Regulatory Architecture

What Are VDAs?

Virtual Digital Assets are electronically stored, transferable digital representations of value. They include:

- Cryptocurrencies — Bitcoin, Ethereum, etc. — secured by cryptographic techniques, resistant to counterfeiting

- NFTs (Non-Fungible Tokens) — unique digital assets recorded on a blockchain, tradeable for money or other assets

- Utility tokens, stablecoins, DeFi instruments — categories that blur the lines between currency, security, and commodity

India’s definitional problem: The term “Virtual Digital Asset” was coined in the Finance Act 2022 purely for taxation purposes. India has never legally defined whether a VDA is a commodity, a security, a currency, or a sui generis (one-of-a-kind) asset class. This definitional gap is the root of every downstream regulatory problem — because which regulator governs VDAs, what investor protections apply, and how courts treat VDA disputes all depend on answering this question first.

- The Income Tax Bill 2025 classifies VDAs as property and capital assets for the first time — aligning India with the UK, US, and Australia — but this is a tax classification only, not a comprehensive legal definition

- Until Parliament passes a framework law, VDAs remain legally orphaned: taxed as property, monitored as a money-laundering risk, but protected by nobody

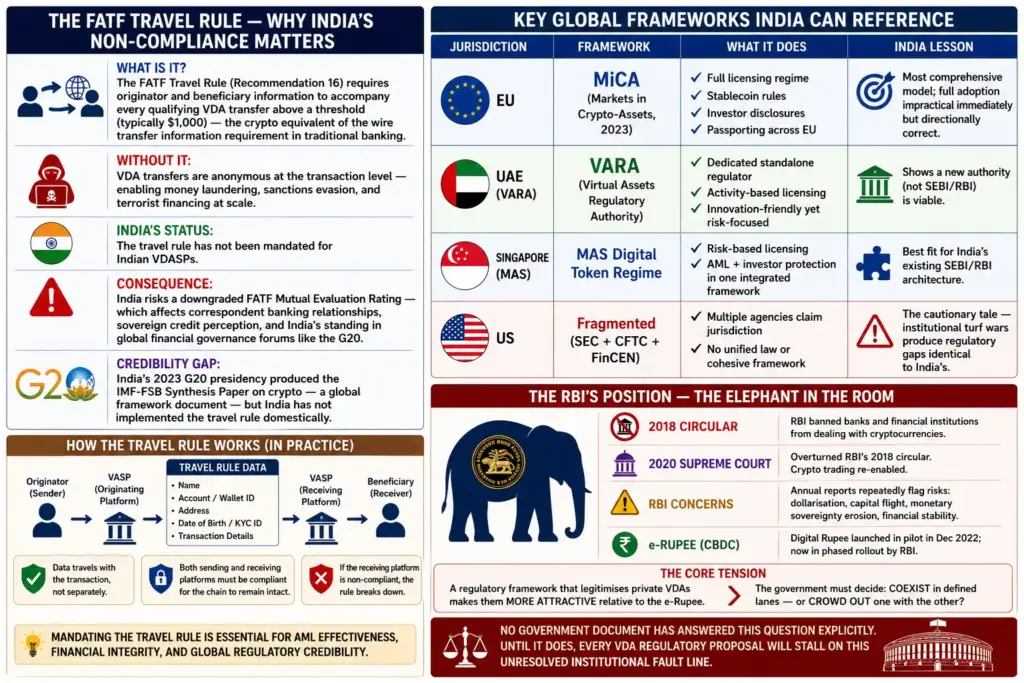

What the “travel rule” means and why it matters:

- The Financial Action Task Force (FATF) Travel Rule requires that originator and beneficiary information accompany every qualifying VDA transfer above a threshold (typically $1,000)

- It is the crypto equivalent of the wire transfer information requirement that traditional banks follow

- Without it, VDA transfers are anonymous at the transaction level — enabling money laundering, sanctions evasion, and fraud at scale

- India has not yet mandated the travel rule — making it non-compliant with FATF’s updated Recommendation 16, which has reputational and correspondent banking consequences

Decoding the Article: Analysis

The 30% Tax + 1% TDS Is Not Neutral Policy. It Has Actively Shaped the Regulatory Vacuum.

- The article mentions the tax regime as one of India’s two VDA pillars — but does not examine how the tax design itself has contributed to the regulatory problem

- The 2022 VDA tax regime was explicitly designed to be discouraging without banning — the government was unwilling to legitimise crypto by regulating it, but also unwilling to ban it outright. The 30% flat tax (no set-off for losses, no distinction between short and long-term gains) and 1% TDS were intended to suppress trading volumes and slow ecosystem growth while the government “decided” on crypto’s legal status

- The unintended consequence: Indian traders migrated to offshore exchanges in large numbers to avoid TDS, because offshore platforms don’t deduct at source. FIU-IND’s October 2025 notices to 25 offshore exchanges and the URL takedown campaign are a direct response to this migration — which the tax design itself caused

- This is a classic policy loop: punitive tax → user migration offshore → offshore platforms escape AML compliance → FIU-IND enforcement campaign → offshore platforms block Indian users → users use VPNs to access them anyway → the problem returns

- The article calls for “balanced taxation” in one line near the end. This is the correct diagnosis but needs to be stated as the root cause of the offshore migration problem, not a secondary consideration. Until the TDS rate is reduced significantly (industry has consistently asked for 0.01–0.05%), the migration pressure will continue and FIU-IND enforcement will remain a game of whack-a-mole with offshore platforms

India Has a Regulatory Sequencing Problem. Industry Practice Cannot Substitute for Legislation, But Legislation Cannot Wait for Industry Practice Either.

- The article’s central strategic recommendation is: let industry build best practices (travel rule compliance, transaction monitoring, grievance redressal) → demonstrate robustness → regulators formally adopt them

- This is a reasonable approach in a stable environment. But it has a sequencing flaw that the article does not identify

- The problem: India’s crypto regulatory window opens and closes with political cycles. The 2021 Cryptocurrency and Regulation of Official Digital Currency Bill — which would have banned private crypto — was listed for Parliament but never introduced, because the government couldn’t build consensus. The 2023 G20 presidency gave India a platform to shape global crypto regulation — but produced a synthesis paper, not domestic legislation. Each time a window appeared to open, it closed before legislation could pass

- Meanwhile, retail users are being harmed right now — the $230 million hack was in 2024, the impersonation case was in 2026. Waiting for industry practice to mature before legislating means more retail harm in the interval

- The correct sequencing is the reverse of what the article proposes: pass a framework law first (even a thin one — defining legal status, establishing a regulator, creating a grievance mechanism), then use delegated legislation (rules and regulations under the framework) to incorporate evolving industry practice. This is how SEBI was built — the SEBI Act 1992 created the framework, and SEBI’s regulations have evolved continuously for 34 years since

- A “SEBI for crypto” — a dedicated VDA authority with rule-making powers — can move faster than Parliament and adapt as technology evolves. The article gestures at this but does not name it as the structural solution

The $230 Million Hack Is Not Just a Consumer Protection Case. It Is a Systemic Risk Signal That India’s Regulators Have Not Priced.

- The article presents the July 2024 exchange hack ($230 million) as a retail harm case — users couldn’t access funds, had no grievance mechanism, had to navigate foreign insolvency proceedings. This framing is correct but incomplete

- $230 million is approximately ₹1,900 crore at 2024 exchange rates — a sum larger than the annual revenue of many mid-sized Indian NBFCs. With 100 million users and growing institutional participation, India’s VDA ecosystem is now large enough to generate systemic risk — not just retail harm

- The specific systemic risk channels that the article does not identify:

- Contagion risk: A large Indian exchange failure (or a large offshore exchange serving Indian users) could trigger simultaneous withdrawal pressure across multiple platforms — the crypto equivalent of a bank run. The 2022 FTX collapse wiped out $32 billion globally and caused cascading failures across the crypto ecosystem. India has no equivalent of the Deposit Insurance and Credit Guarantee Corporation (DICGC) for VDA platforms

- Forex implications: Indian users holding VDAs on offshore platforms represent capital that has effectively left India’s formal financial system without going through RBI’s Liberalised Remittance Scheme (LRS). The scale of this informal capital export is unquantified — but with 100 million users, even modest average balances on offshore platforms represent a material forex position that sits outside RBI’s visibility

- Tax base erosion: The 1% TDS was designed to create a transaction trail for income tax purposes. But with users migrating to offshore platforms to avoid TDS, the Income Tax Department is losing both the withholding and the visibility into gains — creating a growing unreported capital gains problem

- The article frames VDA regulation as an investor protection issue. It is equally a monetary policy, forex management, and systemic risk issue — and the regulator that needs to be at the table is not just SEBI but also the RBI, which has consistently expressed scepticism about private cryptocurrencies while developing the e-Rupee (CBDC)

The Fine Print — What the Article Does Not Fully Address

- The RBI’s position is conspicuously absent from a piece about VDA regulation. The RBI has been the most consistent institutional voice against private cryptocurrencies in India — its annual reports have repeatedly warned of macroeconomic risks from crypto adoption, and it has explicitly stated that private VDAs pose risks to financial stability and monetary sovereignty. Any VDA regulatory framework will require RBI’s buy-in — or a clear legislative decision to override RBI’s objections and place VDA oversight outside RBI’s mandate. The article discusses SEBI, FIU-IND, and Parliament but does not once mention the RBI — which is the single most important institutional actor whose position determines what any VDA law can actually say.

- The e-Rupee (CBDC) creates a direct competitive tension with private VDAs that the article ignores. The RBI has been rolling out the digital rupee (e₹) since December 2022. A comprehensive VDA regulatory framework that legitimises private crypto sits in tension with the RBI’s CBDC ambitions — because a well-regulated, investor-protected VDA ecosystem makes private crypto more attractive relative to the e-Rupee. The government must resolve this tension explicitly: either private VDAs and the e-Rupee coexist in defined lanes (VDAs for investment/speculative use, e-Rupee for payments), or one is meant to crowd out the other. The regulatory framework’s design depends entirely on which choice is made — and the article does not acknowledge this choice exists.

- The Chainalysis “first globally in grassroots adoption” figure needs contextualisation. Chainalysis ranks India first based on a composite index that weights on-chain transaction volume adjusted for purchasing power parity and population. This methodology means India ranks high partly because of its large population and lower PPP base — not necessarily because Indians are the world’s most sophisticated or highest-value crypto participants. The 100 million user figure includes casual users, one-time buyers, and dormant accounts. Active, at-risk retail investors are a subset — important for policy but not 100 million strong. Using this figure without qualification overstates the urgency in one direction while understating the sophistication gap between Indian retail users and the complexity of the products they are accessing.

- The “travel rule” recommendation is correct but operationally harder for India than the article implies. Implementing the FATF Travel Rule requires VDASPs to share originator/beneficiary data with counterparty platforms — but this only works if both the sending and receiving platform are compliant. If an Indian user sends VDAs to a non-compliant offshore wallet, the travel rule breaks down at the receiving end. India has ~25 registered VDASPs with FIU-IND but hundreds of offshore platforms serving Indian users. Until offshore platforms either register with FIU-IND or are effectively blocked (neither of which has been achieved), travel rule compliance by Indian platforms creates a compliance cost without delivering the AML benefit — because the data chain breaks the moment assets move offshore.

- The “ombudsman-like scheme” recommendation is the right idea but needs an anchor regulator first. The article calls for an ombudsman for VDA grievances — similar to the RBI Ombudsman for banking or the Insurance Ombudsman. This is the right retail protection mechanism. But an ombudsman derives authority from a parent regulator. Without first designating which body has primary jurisdiction over VDAs, an ombudsman has no legal standing to adjudicate complaints.

India’s crypto regulatory story is, at its core, a story of institutional hesitation masquerading as caution. Every major economy that has built a credible VDA framework — the EU with MiCA, Singapore with MAS licensing, the UAE with VARA — did so by making a choice: crypto is here, users are exposed, a framework is better than a vacuum. India has spent four years watching retail harm accumulate, user base grow to 100 million, offshore migration accelerate, and courts confirm the jurisdictional gap — while producing tax provisions and AML circulars but no framework law. The $230 million hack is not an argument against crypto; it is an argument for regulation. The impersonation case is not an argument for more FIU-IND notices; it is an argument for a grievance mechanism with statutory teeth. India does not need to choose between innovation and protection — every credible VDA regime in the world has found that formula. What India needs is the political decision to stop choosing neither.

- Sign Up on Practicemock for Updated Current Affairs, Topic Tests and Mini Mocks

- Sign Up Here to Download Free Study Material

Free Mock Tests for the Upcoming Exams

- IBPS PO Free Mock Test

- RBI Grade B Free Mock Test

- IBPS SO Free Mock Test

- NABARD Grade A Free Mock Test

- SSC CGL Free Mock Test

- IBPS Clerk Free Mock Test

- IBPS RRB PO Free Mock Test

- IBPS RRB Clerk Free Mock Test

- RRB NTPC Free Mock Test

- SSC MTS Free Mock Test

- SSC Stenographer Free Mock Test

- GATE Mechanical Free Mock Test

- GATE Civil Free Mock Test

- RRB ALP Free Mock Test

- SSC CPO Free Mock Test

- AFCAT Free Mock Test

- SEBI Grade A Free Mock Test

- IFSCA Grade A Free Mock Test

- RRB JE Free Mock Test

- Free Banking Live Test

- Free SSC Live Test