For aspirants preparing for RBI, SEBI, or NABARD exams, understanding monetary policy decisions is crucial. The April 2026 meeting of the Monetary Policy Committee (MPC) held the repo rate steady at 5.25%, signalling RBI’s balancing act between growth and inflation. This decision comes amid global headwinds—high crude oil prices, a weakening rupee, and trade uncertainty—making it more than just a rate announcement. In this Vishleshan, we decode why the MPC paused its easing cycle, what the inflation and GDP projections mean, and how these choices impact exam‑relevant economic concepts.

Take a Free RBI Grade B Mock Test

RBI MPC meeting April 2026: Repo rate held steady at 5.25%—5 key takeaways from monetary policy decision

Context: When the Reserve Bank of India’s Monetary Policy Committee convenes every six weeks, it doesn’t just set interest rates — it shapes the cost of every home loan, business investment, and rupee borrowed across India. This Mint article unpacks the April 2026 decision examining five key outcomes from the decision.

Link to the Article: Mint

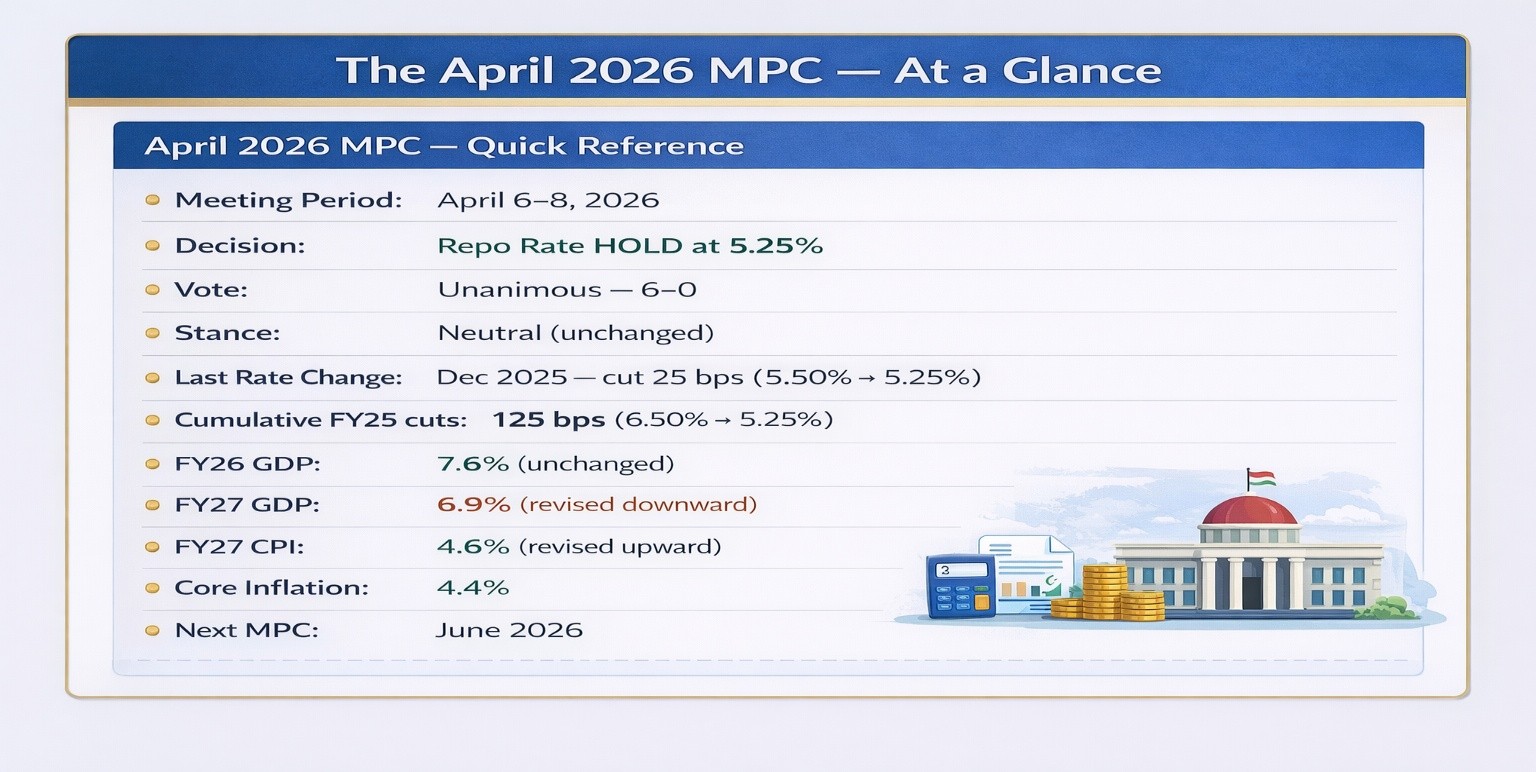

The six-member panel, chaired by Governor Sanjay Malhotra, unanimously kept the repo rate unchanged at 5.25% and retained a neutral policy stance. The decision showed RBI’s effort to balance growth and inflation, with FY27 GDP projected at 6.9% and CPI inflation at 4.6%, while signalling that external risks remain the biggest challenge ahead.

MPC Overview

- The Monetary Policy Committee (MPC) is a six-member statutory body established under Section 45ZB of the RBI Act, 1934 (amended 2016) with a single mandate: keep CPI inflation at 4%, within a tolerance band of 2–6% — a target the Government of India has now retained for 2026–2031.

- Composition: Three RBI officials (Governor chairs) + three external members appointed by the Government of India. Meetings happen six times a year; majority vote binds the institution.

What the MPC Controls

| Rate | Full Form | What It Does | Who It Affects | April 2026 |

| Repo Rate | Repurchase Rate | RBI lends short-term funds to banks against G-Secs | All banks; drives home, personal & MSME loan rates | 5.25% |

| SDF Rate | Standing Deposit Facility Rate | Banks park surplus funds overnight with RBI — no collateral | Banks with excess liquidity; floor of LAF corridor | 5.00% |

| MSF Rate | Marginal Standing Facility Rate | Emergency overnight borrowing for banks facing fund crunches | Banks; ceiling of the LAF corridor | 5.50% |

| Bank Rate | Long-Term Lending Rate | RBI lends long-term; benchmark for penal charges on banks | Long-term lending benchmark; moves with MSF | 5.50% |

The April 2026 MPC — At a Glance

In April 2026, this committee met against a backdrop of $100+ crude oil, a weakening rupee, and mounting global trade uncertainty — making the rate decision more consequential than the number alone suggests

Decoding the Article – Analysis and What’s Next

Let’s decode the decision in three layers:

Decoding the Decision in three layers

Layer 1: Why Not Cut?

The MPC’s 125 bps rate-cut cycle (Feb–Dec 2025) is paused, but 20 bps of that easing is still transmitting to actual loan rates. Cutting further won’t fix $100+ crude oil — an external supply shock. Cheaper credit would mechanically boost demand and worsen inflation. By holding steady, the RBI also calms bond markets where 10-year G-Sec yields have approached 7%, near a 16-month high.

Layer 2: Inflation Picture

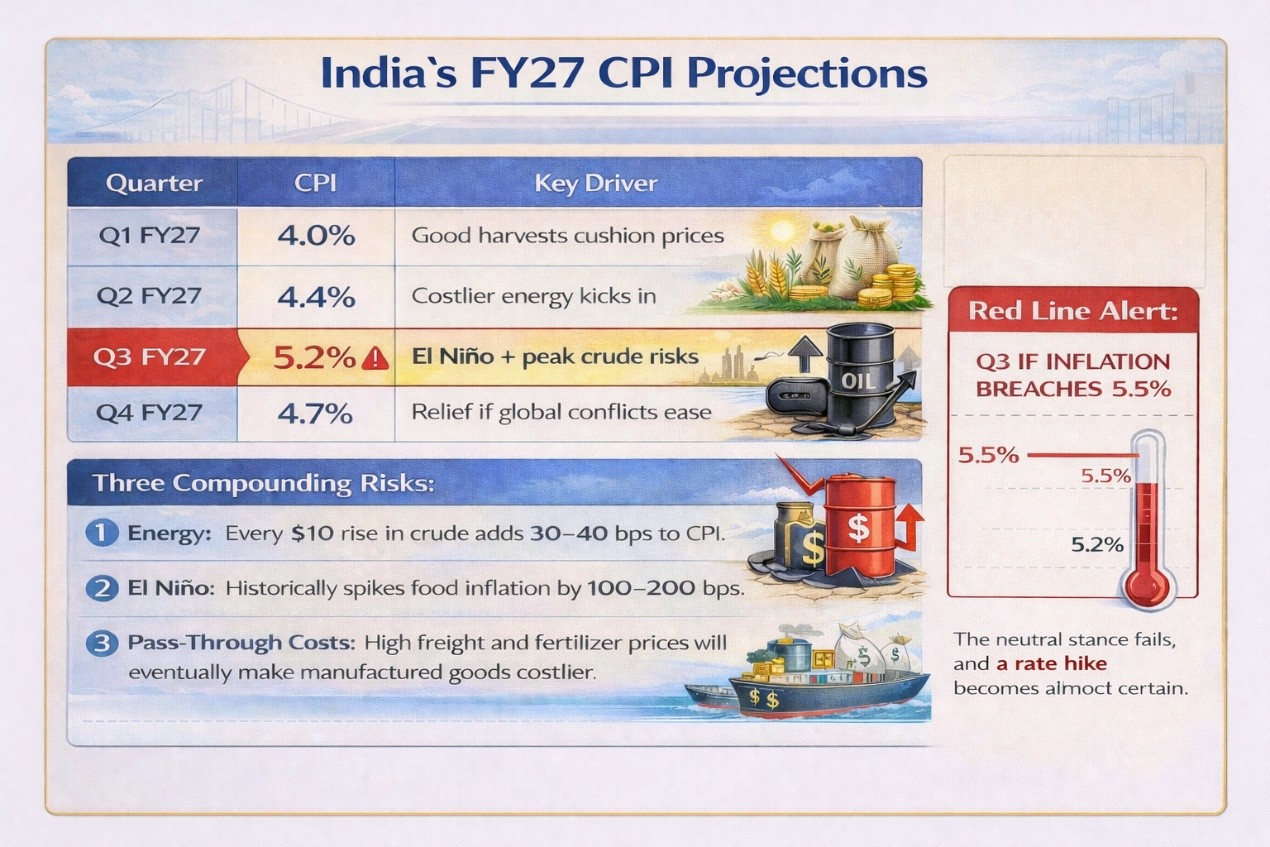

Overall FY27 CPI is projected at 4.6%, but core inflation at 4.4% signals underlying demand pressure. The quarterly breakdown reveals a dip-and-recovery pattern driven entirely by external forces — with Q3 FY27 at 5.2% marking the sharpest risk zone.

Layer 3: GDP Revision

India’s FY27 GDP is revised to 6.9% from FY26’s 7.6% — not due to domestic weakness, as private consumption, manufacturing, and government capex remain strong, but entirely because of external headwinds: weaker global trade and FPI outflows. One underappreciated risk is remittances. India’s record $125 billion inflow in FY25 faces pressure from the West Asia conflict, which could disrupt flows from the Gulf region.

What a Steady Repo Rate Does to the Indian Economy

| # | Who Is Affected | What happens | What It Means |

| 1 | Home Loan Borrowers | EMIs stay the same | No savings on monthly payments, but no increase either. Millions of borrowers stay at current rates. |

| 2 | Bank Borrowers & Businesses | Loans stay at current cost | Credit keeps flowing at the same pace — the system doesn’t slow down or speed up. |

| 3 | Every Indian Consumer | Prices stay more controlled | RBI is not adding cheap money into a market where oil is already expensive. That prevents further price rise. |

| 4 | FD Holders & Senior Citizens | FD interest rates are protected | Banks won’t cut deposit rates. A ₹10 lakh FD earning 7% still earns ₹70,000/year. |

| 5 | Importers & Common Public | Rupee stays stable | India’s higher interest rate keeps foreign investors from pulling money out. A weaker rupee means costlier petrol, oil, and electronics — the hold prevents that. |

| 6 | Businesses & MSMEs | Planning becomes easier | Companies know the cost of borrowing won’t change suddenly. That confidence drives investment decisions. |

| 7 | Government & Taxpayers | Government saves money | At ₹17.2 lakh crore of borrowing, even a 25 bps rate rise would cost the government an estimated ₹4,300 crore extra annually |

The Structural Measures That Matter Most

These four structural moves deserve more attention than the rate decision itself

1. Rationalising Bank Board Oversight

The issue: India’s bank boards spend a disproportionate share of their time approving routine regulatory matters that don’t require board-level attention — an artefact of outdated rules.

What RBI is doing: After a comprehensive review, RBI will streamline the list of matters requiring Board approval. Routine decisions will be delegated downward, freeing Boards to focus on credit policy, risk management, and capital allocation.

Why it matters: Governance efficiency directly affects the speed of banking decisions — from loan approvals to risk escalations. Lighter board agendas mean sharper strategic focus.

2. 9,000 Instructions Condensed into 238 Master Directions

The issue: India’s banking regulation has grown layer by layer over 70 years. By April 2026, banks were navigating over 9,000 individual regulatory instructions — many overlapping, some contradictory, most requiring a legal team to interpret.

What RBI has done: Completed a consolidation exercise, compressing all 9,000+ instructions into 238 Master Directions — one clear, unified rulebook. A parallel exercise covers supervisory instructions too.

Why it matters: Compliance costs fall. Smaller banks and NBFCs — who can’t afford large legal teams — gain equal footing with large institutions.

3. MSME TReDS Onboarding — Due Diligence Removed

What is TReDS? The Trade Receivables Discounting System is an RBI-regulated digital platform where MSMEs upload unpaid invoices and get paid immediately by banks — instead of waiting 60–90 days for buyers to pay. It directly solves India’s biggest MSME problem: cash flow stress.

The problem: MSMEs had to complete a due diligence process — documents, verifications, approvals — that acted as a time-consuming barrier for smaller businesses.

What RBI has done: The due diligence requirement for MSME onboarding on TReDS has been removed entirely.

Why it matters: India has over Over 7.83 crore enterprises (Udyam portal). Most run on thin margins and face constant working capital pressure. For a small manufacturer waiting 75 days for a large buyer to pay an invoice, faster TReDS access is the difference between surviving the month and not.

4. Opening the Term Money Market to NBFCs, AIFs, and HFCs

What is the term money market? The short-term interbank market where institutions borrow and lend money for fixed periods — typically 1 to 14 days. Until now, only banks and Standalone Primary Dealers (SPDs) could participate.

What RBI is doing: Opening this market to Non-Banking Finance Companies (NBFCs), Alternative Investment Funds (AIFs), and Housing Finance Companies (HFCs).

| Step | What Happens | End Result |

| 1. NBFCs get market access | NBFCs can now borrow directly in the short-term interbank market | No longer dependent on expensive bank borrowing alone |

| 2. Funding costs fall | Short-term borrowing becomes cheaper for NBFCs | Cost of running their loan books reduces significantly |

| 3. Savings passed to borrowers | NBFCs price their loans lower | MSME loans, vehicle loans, and home loans become cheaper for end borrowers |

| 4. SPD borrowing limit rises | Standalone Primary Dealers can borrow more in the term market | Government securities market becomes deeper, more liquid, and more stable |

The One Number That Defines FY27

RBI’s own projection of 5.2% CPI in Q3 FY27 signals that the second half carries real price risk.

Three scenarios follow from here:

| Scenario | Trigger | MPC Response |

| Extended hold | Oil <$90, El Niño mild | Status quo through FY27 |

| Rate cut | Conflict eases, GDP <6.5% | 25 bps cut, H2 FY27 |

| Defensive hike | Oil >$110, CPI >5.5%, rupee >₹97 | Hike to protect the band |

The 125 bps easing cycle is almost certainly over. Markets that priced further cuts are now repricing — and that repricing alone tightens financial conditions, even without a single hike.

Forward Outlook: June Decides the Direction

The June 2026 MPC hinges on two data points: the May CPI print and the IMD monsoon forecast. If El Niño is confirmed as a deficient-monsoon year, food inflation risk in Q3 becomes RBI’s dominant concern — and any remaining cut expectations would likely recede sharply. For the average Indian, April’s hold means: loans stay at current rates, deposits remain rewarding, and the rupee holds its floor.

The economy moves forward on momentum already built, not borrowed acceleration.

- Sign Up on Practicemock for Updated Current Affairs, Topic Tests and Mini Mocks

- Sign Up Here to Download Free Study Material

Free Mock Tests for the Upcoming Exams

- IBPS PO Free Mock Test

- RBI Grade B Free Mock Test

- IBPS SO Free Mock Test

- NABARD Grade A Free Mock Test

- SSC CGL Free Mock Test

- IBPS Clerk Free Mock Test

- IBPS RRB PO Free Mock Test

- IBPS RRB Clerk Free Mock Test

- RRB NTPC Free Mock Test

- SSC MTS Free Mock Test

- SSC Stenographer Free Mock Test

- GATE Mechanical Free Mock Test

- GATE Civil Free Mock Test

- RRB ALP Free Mock Test

- SSC CPO Free Mock Test

- AFCAT Free Mock Test

- SEBI Grade A Free Mock Test

- IFSCA Grade A Free Mock Test

- RRB JE Free Mock Test

- Free Banking Live Test

- Free SSC Live Test