For policymakers tracking India’s energy security, the April 2026 developments offer more than a geopolitical headline. Yes, the US sanctions waiver on Russian crude has expired, but the real story lies beneath—India’s continued reliance on Russian oil, a deepening LPG supply shock, and a fragile import architecture exposed by the Strait of Hormuz disruption. These shifts reveal structural vulnerabilities that a single policy decision cannot capture. Is India navigating a temporary supply disruption, or confronting a deeper energy security crisis shaped by geopolitics and infrastructure gaps? In this Vishleshan, we decode India’s post-waiver strategy, unpack three critical layers of risk, and outline the reforms needed to future-proof the country’s energy supply chain.

India to continue buying Russian crude, LPG despite end of US sanctions waiver

Context: When West Asia shut down, India’s energy system faced its sharpest stress test in a generation. For 340 million households that light their stoves with an LPG cylinder every morning, this was not a geopolitical event — it was a kitchen crisis. New Delhi responded the way it almost always does: quietly, without apology, and without asking anyone’s permission. It turned to Moscow. The US waiver that briefly legitimised those Russian barrels is now gone. India’s position is unchanged.

Link to the Article: Mint

India’s Energy Import Architecture Background

Before the West Asia war broke, India’s energy import map looked like this:

- India imports 85%+ of its crude oil requirement — making it the world’s third-largest oil importer after the US and China

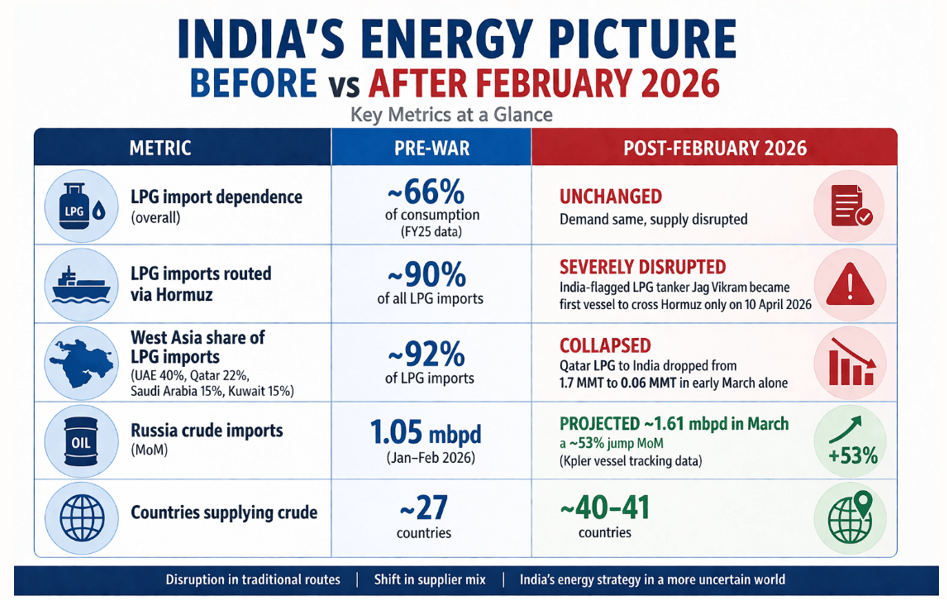

- LPG imports meet ~65% of India’s total annual consumption of 33 million tonnes — covering the cooking fuel of 340 million households

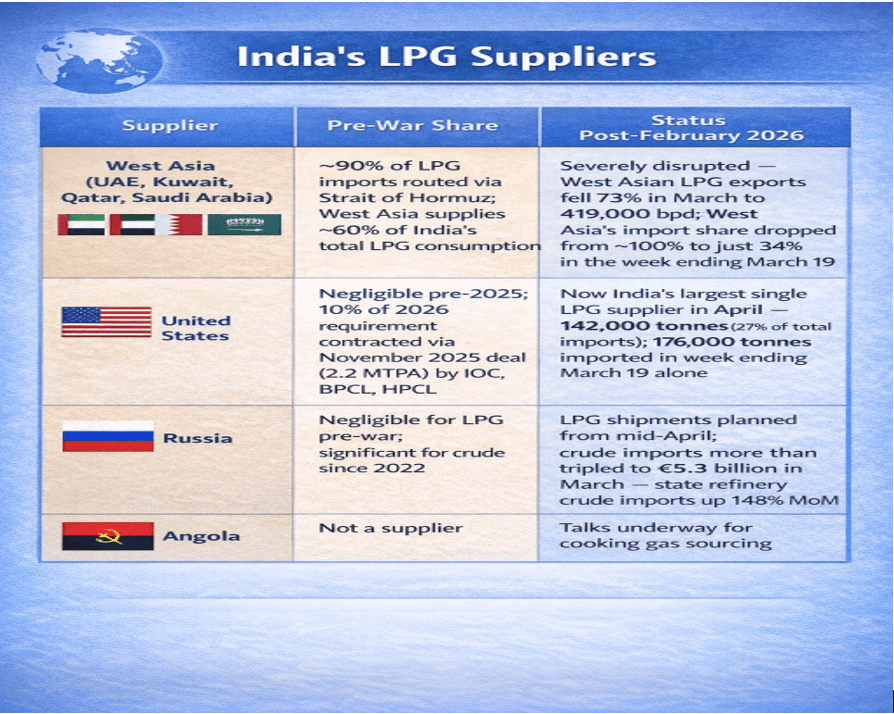

- Of these LPG imports, 90% were routed through the Strait of Hormuz — the 34-km-wide chokepoint between Iran and Oman that became a war zone on 28 February 2026

- India sources crude from 41 countries today (up from 27 a few years ago) and LPG from 16 countries (up from 10), but diversification on paper did not prevent concentration in practice

India’s LPG Import Dependency: Country Breakdown

The US Sanctions Waiver — What Expired and Why It Matters

What Are US Sanctions on Russian Oil?

- Post-Ukraine invasion (Feb 2022), the US, EU, and Western allies imposed sanctions on Russian oil exports to cut Moscow’s war revenues

- Key restrictions: blocked global financial transactions for Russian crude, denied Western shipping insurance to Russian oil tankers, and imposed a $60/barrel price cap on Russian exports

- India continued importing Russian oil via legal workarounds — rupee/dirham payments, non-Western ships, non-Western insurance — from entities not directly sanctioned

- Result: without a single formal waiver, Russia became India’s largest crude oil supplier — and stayed there for three years.

Why the West Asia War Created a New Crisis

- On 28 February 2026, the US-Iran war erupted and Iran restricted Strait of Hormuz shipping.

- Hormuz carries ~20% of global crude and LPG — India’s primary import route was suddenly choked.

- West Asia had supplied ~60% of India’s crude pre-war; that share collapsed overnight

- Russian tankers with loaded crude sat idle at sea — available, cheap, and in search of buyers

What the US Treasury Did

- On 5 March 2026, US Treasury issued a General Licence — a temporary, formal waiver — covering Russian crude already loaded onto vessels by March 12, provided it was bought by Indian firms

- India responded instantly: IOC bought ~10 mn barrels, Reliance ~10 mn barrels and total ~30 mn barrels secured within days. These tankers turned around mid-sea toward Indian ports

- Waiver validity: 5 March – 11 April 2026 (30 days)

What Expired on 11 April 2026

| What Expired | What Did NOT Expire |

| Legal permission to buy Russian crude loaded before March 12 | India’s non-sanctioned entity import route |

| Spot market access to waiver-covered transit cargoes | Rupee/dirham payment mechanisms |

| US formal tolerance for those specific barrels | Decades-old India-Russia energy trade structure |

India’s Position

When the waiver expired on 11 April, India’s response was measured and unhesitating. India has been buying Russian crude since 2022, through three years of Western pressure, without any formal permission. The March 2026 licence was an exception to that arrangement, not its foundation. India’s actual structural basis for Russia trade is the non-sanctioned entity route — purchases routed through Russian producers and intermediaries not named on any sanctions list, paid in rupees or dirhams, shipped on non-Western vessels, and insured by non-Western providers. This architecture predates the waiver, survived it, and continues after it.

Why the Expiry Still Matters — 3 Consequences

- Diplomatic signal — Washington’s tolerance for Russian energy trade has limits; India must account for this in its US relationship

- Transaction risk — Grey zones narrow; any accidental link to a sanctioned entity now carries higher secondary sanctions exposure

- Price impact — During the waiver window, discounted Russian barrels flooded the spot market, suppressing the price India paid. With sanctions back in full force and spot availability tightening, India’s average Russian crude purchase price will likely edge upward — a modest but real fiscal cost that flows directly into refinery margins and, eventually, retail fuel prices.

Article Decoding: Three Layers Beyond the Headline

Layer 1 — The Crude Shift: Russia Fills the West Asia Gap

- West Asia accounted for ~60% of India’s crude oil imports before the war broke out on 28 February 2026. That share has now fallen to ~30%

- Russian crude imports doubled month-on-month in March, according to CREA (Centre for Research on Energy and Clean Air)

- India was the second-highest buyer of Russian fossil fuels in March after China — importing €5.8 billion worth of Russian hydrocarbons

- State-owned refineries alone saw a 148% surge in Russian imports, driven by the spot market availability of Russian barrels at commercially attractive prices

- When primary source drops from 60% to 30%, Russia filled the gap. Russia was available, non-sanctioned entities were accessible, and the price worked.

Layer 2 — The LPG Crisis: 340 Million Households on the Edge

- India’s LPG crisis is not an energy-security abstraction — it is a kitchen crisis for 34 crore households that use cylinder gas as their primary cooking fuel

- With 90% of LPG imports dependent on the Hormuz route, the war-driven disruption hit domestic supply almost immediately

- The government invoked emergency measures: directing refiners to ramp up domestic LPG production, prioritising household supplies over commercial demand, and activating the Essential Commodities Act

- Despite these measures, panic booking surged across the country and long queues were witnessed outside LPG distribution centres in multiple states

Layer 3 — The Geopolitical Tightrope: India Between Washington and Moscow

- The US signed a deal in November 2025 to supply 10% of India’s total LPG requirement in 2026 — making it both a sanctions enforcer and India’s primary energy backup.

- India’s response is calibrated: import from Russia via non-sanctioned entities, maintain the US as the primary LPG anchor, diversify to Canada, Australia, Angola, and Japan — and say nothing provocative publicly

- What makes April 2026 structurally different from 2022 is that India now faces a genuinely contradictory position: its largest LPG backup supplier (the US) and its largest crude supplier (Russia) are on opposite sides of a sanctions regime.

The Big Number: 90%: India imports LPG from 16 countries and crude from 41 — the diversification looks impressive on paper, until you notice that 90% of those imports were funnelled through a single 34-kilometre chokepoint(Strait of Hormuz). That is not energy diversification. That is a single-point-of-failure dependency with extra steps — and the Strait of Hormuz just proved it.

Action Agenda

| # | Area | Problem | Solution |

| 1 | Route Diversification | 90% of LPG imports flowed through a single 34-km chokepoint. India has already pivoted to Cape of Good Hope routing as a crisis workaround — but a workaround is not a strategy. | Formalise Cape of Good Hope routing through long-term LPG carrier contracts and direct bypass agreements with the US, Australia, and Russia. Do not let this routing revert to Hormuz the moment the crisis eases — the next closure will come. |

| 2 | Strategic LPG Reserve | India’s existing crude SPR covers only ~9–10 days of import needs — already well below the IEA’s 90-day benchmark. For LPG, the buffer is zero. When Hormuz closed, India had no cushion at all. | Build dedicated LPG strategic storage — minimum 30 days of import cover — modelled on crude SPR facilities at Visakhapatnam, Mangalore, and Padur. Without this, every West Asia crisis becomes a household crisis within days.. |

| 3 | Domestic LPG Production | India’s domestic refinery LPG output covers only ~35% of demand. Refinery capacity expansion for LPG has been consistently deprioritised — treated as a byproduct problem, not an energy security problem. | Incentivise dedicated LPG extraction units at existing refineries and accelerate petrochemical integration that co-produces LPG as a byproduct. Set a binding domestic coverage target of 50% by FY29. Every tonne produced domestically is one tonne that cannot be held hostage by a geopolitical crisis 4,000 km away. |

| 4 | US-India LPG Partnership | The November 2025 US-India LPG deal covers 10% of demand — useful in peacetime, inadequate in a crisis. Canada and Australia remain in informal talks with no signed agreements and no supply triggers. | Formalise multi-year LPG supply contracts with the US, Canada, and Australia — with floor volume commitments, penalty clauses, and pre-positioned cargoes in Indian ports. Spot market purchases work in peacetime. In a disruption, only contracts with activation triggers provide real security. |

| 5 | Demand-Side Substitution | 340 million households depend entirely on cylinder LPG with no cooking fuel alternative. Demand concentration is as dangerous as supply concentration — yet policy has consistently ignored this side of the equation. | Accelerate Piped Natural Gas (PNG) rollout to Tier-2 and Tier-3 cities. Introduce targeted subsidies for induction cooking adoption among Ujjwala beneficiaries and low-income urban households. Every household shifted to PNG or induction permanently shrinks India’s Hormuz exposure — not through better supply management, but through less demand. |

What to Watch

The immediate test is whether the 800,000 tonnes of LPG contracted from Russia, Australia, and the US reaches Indian ports in time to relieve the distribution stress. The RBI is watching this too — LPG price pass-through into CPI is the single variable most capable of derailing the FY27 inflation trajectory of 4.6%.

Three indicators to watch over the next quarter:

- Does the West Asia conflict ease enough to reopen Hormuz-routed shipping by Q2 FY27?

- Does the US-India LPG deal scale beyond 10% of requirement to a formal strategic supply partnership?

- Does India’s domestic LPG production ramp-up — directed by the government — show up in PPAC data as a structural increase, or reverse once the crisis eases?

- Sign Up on Practicemock for Updated Current Affairs, Topic Tests and Mini Mocks

- Sign Up Here to Download Free Study Material

Free Mock Tests for the Upcoming Exams

- IBPS PO Free Mock Test

- RBI Grade B Free Mock Test

- IBPS SO Free Mock Test

- NABARD Grade A Free Mock Test

- SSC CGL Free Mock Test

- IBPS Clerk Free Mock Test

- IBPS RRB PO Free Mock Test

- IBPS RRB Clerk Free Mock Test

- RRB NTPC Free Mock Test

- SSC MTS Free Mock Test

- SSC Stenographer Free Mock Test

- GATE Mechanical Free Mock Test

- GATE Civil Free Mock Test

- RRB ALP Free Mock Test

- SSC CPO Free Mock Test

- AFCAT Free Mock Test

- SEBI Grade A Free Mock Test

- IFSCA Grade A Free Mock Test

- RRB JE Free Mock Test

- Free Banking Live Test

- Free SSC Live Test