For aspirants preparing for RBI, SEBI, or NABARD exams, staying updated on fiscal reforms is essential. One of the most significant recent changes is the Centre’s shift to demand‑based fund release under the SNA‑Sparsh system. This reform is not just about spending efficiency—it’s about strengthening India’s fiscal discipline. In this edition of Vishleshan, we break down how this new model is transforming fund flows, why it matters for competitive exams, and what candidates must understand to stay ahead.

Take a Free RBI Grade B Mock Test

How demand-based fund release is improving the Centre’s fiscal discipline

Context: There is a quiet but important shift in India’s fiscal management: the Centre is no longer releasing scheme funds in advance, but only when payments are actually due. This Mint explainer argues that fiscal discipline is now being enforced in real time — one payment instruction at a time.

Link to the Article: Mint

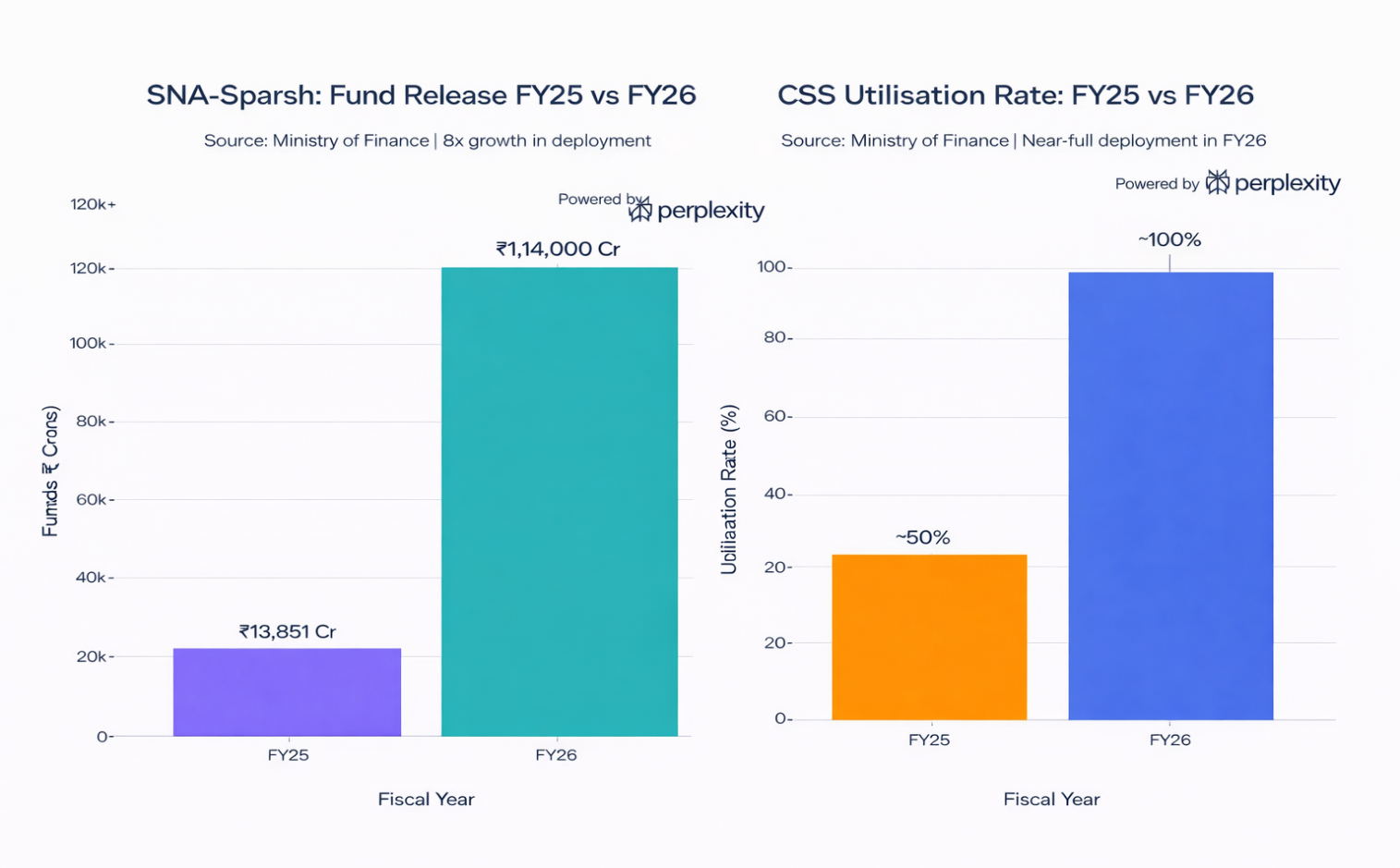

For decades, India’s fiscal shortfall was not a failure of budgetary ambition, but a failure of plumbing that left allocated funds stranded. SNA-Sparsh is the structural fix to this execution gap, redesigning how public money flows rather than just what gets funded. With ₹1.14 trillion deployed at near-100% utilisation in FY26, the immediate repair is a proven success — leaving FY27 to test its resilience at scale.

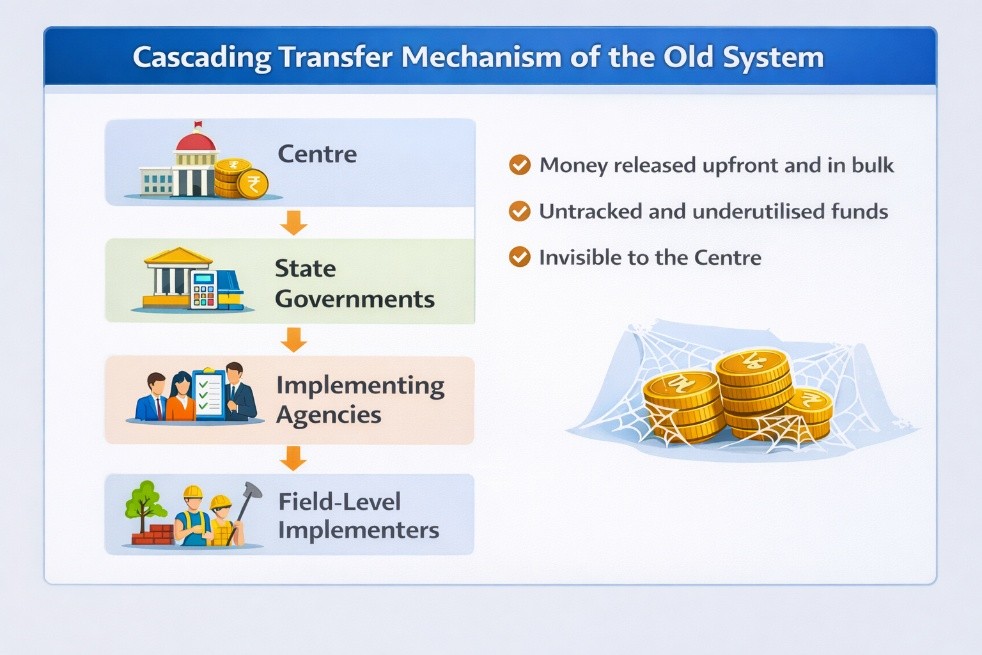

The Problem That Went Unnoticed for Decades

- India’s Centrally Sponsored Schemes (CSS) are shared-expenditure programmes where the Centre and states split costs — typically in a 60:40 ratio, or 90:10 for special category states.

- The Centre allocated ₹5.41 lakh crore for CSS in FY26, roughly 50% of total capital expenditure, covering programmes like PM Awas Yojana, National Health Mission, MGNREGS, and Samagra Shiksha. This is the single largest pipeline through which government money reaches citizens.

- For decades, this pipeline leaked — not because of corruption alone, but because of design.

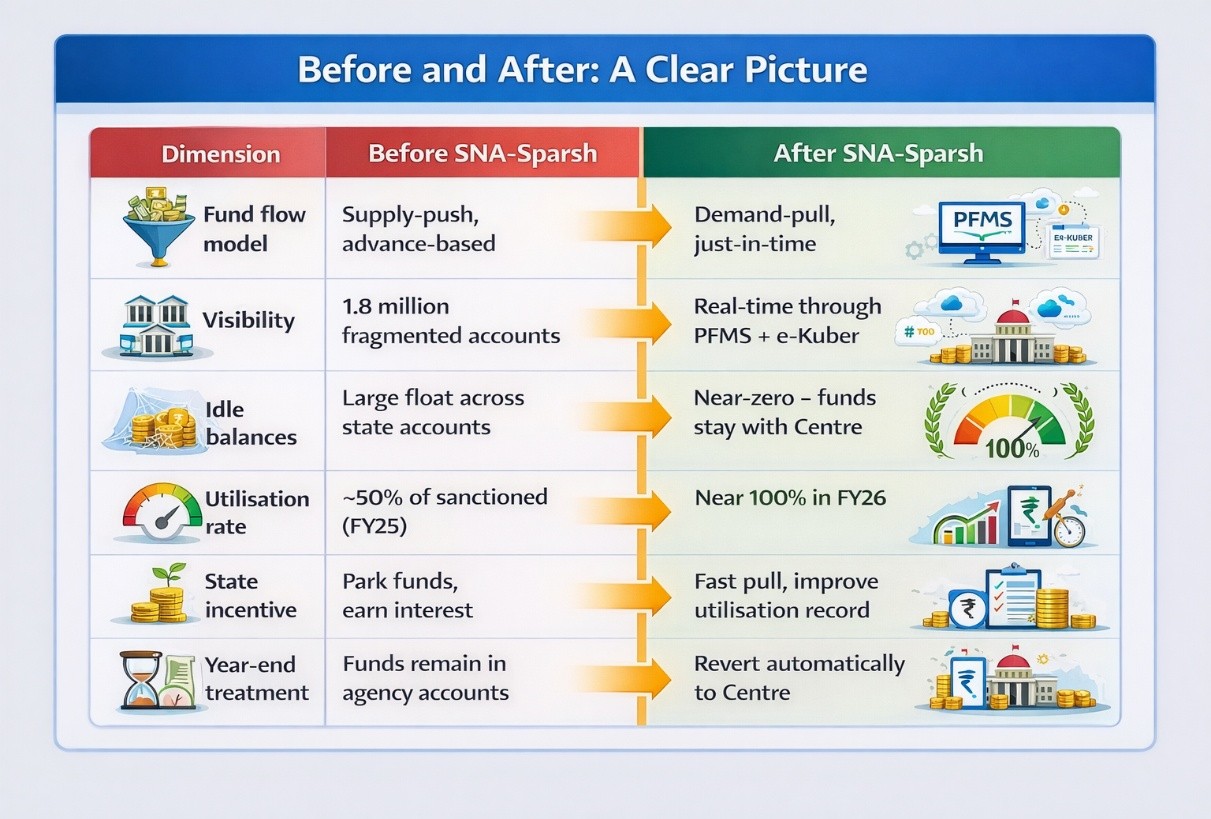

- Before the 2021 SNA reforms, implementing agencies held funds across more than 1.5 million government bank accounts. There was no real-time visibility into utilisation. A rupee released by a central ministry could sit in a district-level account for months — with no mechanism to flag it.

- States had a perverse incentive to let this continue. Parked CSS funds earned interest income, giving state treasuries informal short-term liquidity. Every idle rupee was, in effect, a free loan from the Centre.

- The consequence was measurable. In FY25, against a mother sanction of ₹24,369 crore, only ₹13,851 crore — roughly 50% — was actually released. Half the sanctioned money never reached its destination.

- This was not an anomaly. It was the system working exactly as designed.

SNA-Sparsh Overview

SNA-Sparsh stands for Single Nodal Agency – Samayochit Pranali Ekikrit Shighra Hastantaran. Funds are released only when they are actually needed.

It arrived in two phases:

- Phase 1 (July 2021): 1.8 million implementing agency bank accounts were consolidated into just 4,500 SNA accounts — one per scheme per state. This single move generated projected annual savings of USD 1.2 billion by reducing idle balances. But Phase 1 was still advance-based. Money moved in bulk, just through fewer accounts.

- Phase 2 — SNA-Sparsh: The critical upgrade. A “pull” mechanism was added — funds move only when payment instructions are actually generated by state systems. The Centre’s money stays with the Centre until the exact moment it is needed. From November 1, 2025, this became mandatory for all CSS.

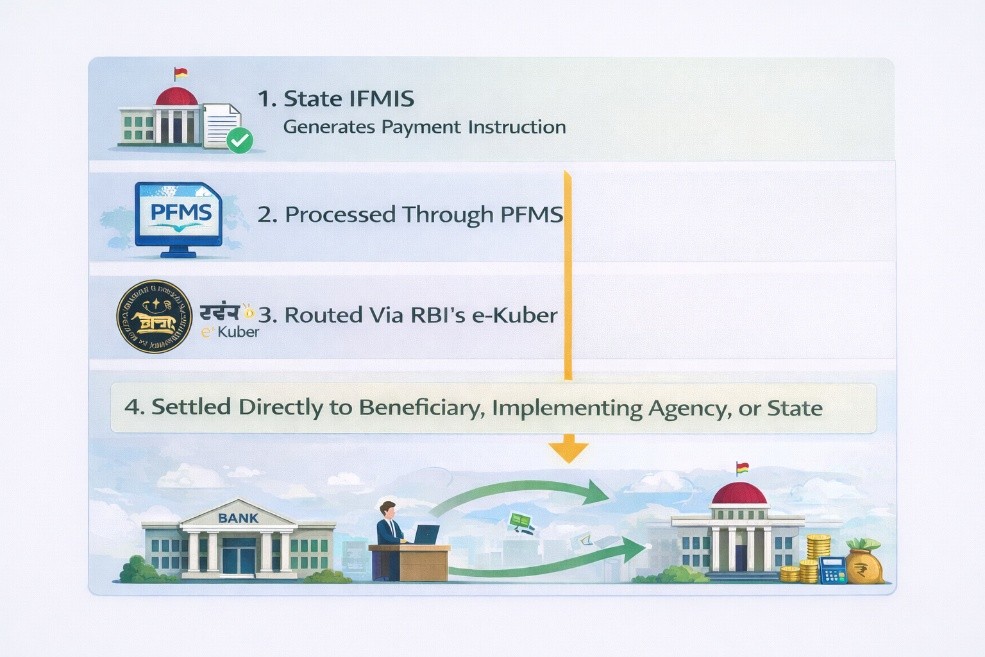

How the SNA-Sparsh Works

RBI becomes the sole banking channel for all CSS fund flows, eliminating the commercial bank intermediaries that previously earned float income on government money. Unutilised funds at year-end automatically revert to the Centre — no more year-end parking, no more carry-forward balances quietly inflating state accounts.

The fund flow under SNA-Sparsh follows a precise, auditable path:

Why This Is a Borrowing Reform, Not Just a Spending Reform

- Most coverage of SNA-Sparsh focuses on fund utilisation, but the more consequential impact is on the Centre’s borrowing programme.

- By releasing funds only when needed, the government avoids advance borrowing — saving over ₹11,000 crore in interest costs since FY2023, with no expenditure cuts, new taxes, or legislative changes required.

- SNA-Sparsh is fiscal discipline through process design: it changes only the timing of when money moves, and that single change does some of the heaviest lifting in India’s fiscal consolidation.

The Numbers That Validate the Model

The Way Forward —What Needs to Be Done

| Area | Problem | Solution |

| State treasury infrastructure | Not all states have strong IFMIS systems. This can slow payments and create uneven results. | Upgrade weaker state treasury systems through targeted support and capacity building. |

| Scheme coverage | Some smaller CSS schemes are still outside SNA-Sparsh. That allows old fund flow problems to continue. | Bring all remaining schemes under SNA-Sparsh with a fixed rollout timeline. |

| Accountability | The system tracks spending, but not actual outcomes. That weakens oversight. | Link fund release to real-time progress and output tracking. |

| State flexibility | A uniform model may not suit every state. Local conditions can differ widely. | Allow states limited flexibility within a clear accountability framework. |

| Centre-state coordination | Faster transfers can still face delays if state systems are not aligned. | Set up a formal coordination mechanism between PFMS and state finance departments. |

What to Watch

The Finance Ministry has mandated SNA-Sparsh across all CSS from November 2025 — and FY27 will be the real stress test: whether near-100% utilisation holds as the system expands to more complex schemes with larger beneficiary bases. Beyond India’s borders, PFMS-based tools including SNA-Sparsh are being shared with countries across Africa, Latin America, and Asia, with the IMF singling it out as a global model for just-in-time fiscal transfers.

- Sign Up on Practicemock for Updated Current Affairs, Topic Tests and Mini Mocks

- Sign Up Here to Download Free Study Material

Free Mock Tests for the Upcoming Exams

- IBPS PO Free Mock Test

- RBI Grade B Free Mock Test

- IBPS SO Free Mock Test

- NABARD Grade A Free Mock Test

- SSC CGL Free Mock Test

- IBPS Clerk Free Mock Test

- IBPS RRB PO Free Mock Test

- IBPS RRB Clerk Free Mock Test

- RRB NTPC Free Mock Test

- SSC MTS Free Mock Test

- SSC Stenographer Free Mock Test

- GATE Mechanical Free Mock Test

- GATE Civil Free Mock Test

- RRB ALP Free Mock Test

- SSC CPO Free Mock Test

- AFCAT Free Mock Test

- SEBI Grade A Free Mock Test

- IFSCA Grade A Free Mock Test

- RRB JE Free Mock Test

- Free Banking Live Test

- Free SSC Live Test