For economists and policymakers tracking India’s growth story, the February–March 2026 GDP revisions offer far more than a routine statistical update. Yes, the base year shift to 2022–23 and downward revisions to recent growth rates have grabbed headlines, but the real story lies beneath—an intensifying debate over overstated output, a persistent blind spot in measuring the informal economy, and methodological tensions in how inflation is accounted for. These are not isolated statistical quirks; they point to deeper questions about how accurately India’s economic reality is being captured. Is this merely a technical recalibration of national accounts, or a signal of structural cracks in the way growth itself is measured? In this Vishleshan, we unpack the 2026 GDP overhaul, decode three core debates shaping the credibility of India’s data, and examine what must change to build a more reliable economic ledger.

Modernizing the ledger: Inside the quest to solidify India’s economic data

Context: Numbers that define a nation’s economic health should be beyond reasonable doubt. India’s GDP number, for most of the last decade, was not. This Mint article — published April 19, 2026 by HowIndiaLives.com — traces a decade-long reckoning with how India measures its own economy, what the new 2026 revision actually changes, and whether the uncomfortable gap between official growth and lived reality has finally been addressed.

Link to Article: Mint

In February 2026, India released a new GDP series with a revised base year of 2022–23. The revisions were significant — real GDP growth for FY24, FY25, and FY26 was revised downward from 9.2%, 6.5%, and 7.4% to 7.2%, 7.1%, and 7.6% respectively. Simultaneously, a paper by researchers Anand, Felman, and Subramanian — published by the Peterson Institute for International Economics in March 2026, safter the revision — argued GDP had been overstated by over one-fifth and consumption by nearly one-third, triggering one of the sharpest official rebuttals in recent Indian economic history.

GDP Measurement: Background

GDP — Gross Domestic Product — is the total monetary value of all goods and services produced in an economy in a given year, measured at market prices. It is used to determine fiscal deficit ratios, current account deficit ratios, debt sustainability, investment attractiveness, and global rankings. A 1% error in GDP measurement is not a statistical footnote — it changes billions of dollars in perception and policy.

India calculates GDP through three approaches:

| Approach | What It Measures | India’s Primary Use |

| Production/Output Approach | Value added at each stage of production | Primary — via Gross Value Added (GVA) |

| Expenditure Approach | Consumption + investment + government spend + net exports | Cross-check |

| Income Approach | Sum of all incomes earned in the economy | Limited use |

India has updated its GDP base year from 2011–12 to 2022–23, replacing an outdated benchmark last revised in 2015. This makes growth estimates more realistic by reflecting today’s economy shaped by post-COVID recovery, GST, and the UPI-driven digital shift. The new series also introduces double deflation in manufacturing, a better method that separately tracks input and output prices for more accurate measurement.

What the Revision Actually Changed

The 2026 revision is the most comprehensive overhaul of India’s national accounts in over a decade, covering five dimensions:

| Reform Area | What Changed |

| Base year | Shifted from 2011–12 to 2022–23 |

| Informal sector measurement | New survey data from Survey of Unincorporated Enterprises 2023–24 |

| Services sector | Expanded coverage using GST data and digital payment footprints |

| Labour market statistics | Integrated PLFS (Periodic Labour Force Survey) data |

| Price deflation | Double deflation introduced; 500+ sector-specific price indicators used |

In absolute terms, nominal GDP for FY26 came in at ₹345.47 trillion — ₹11.67 trillion lower than the old estimate of ₹357.14 trillion. Nominal GDP for FY24, FY25, and FY26 was revised down by 2.9–3.8% across the board.

Decoding the Article

Debate 1: Did the Old Series Overstate Growth?

The Anand-Felman-Subramanian paper — published through the Peterson Institute for International Economics in March 2026 — argues that India’s 2025 GDP levels are overstated by over one-fifth, and consumption by nearly one-third.

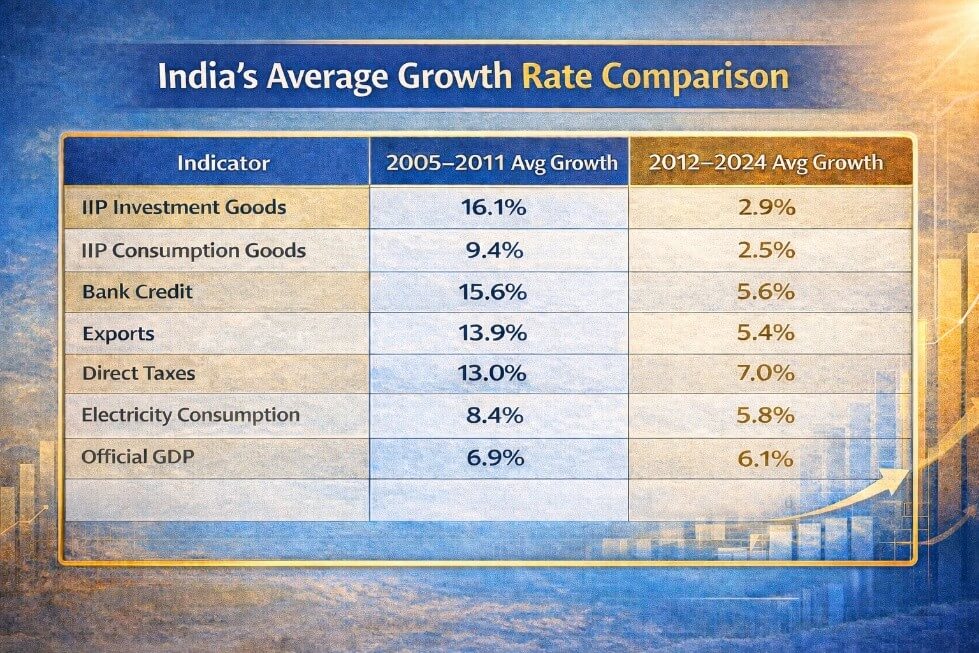

When they apply their corrections, GVA growth between 2011 and 2023 drops from the official 5.9% per year to just 4.0–4.4%. Their primary evidence is a clean and clear one: after 2012, GDP growth barely budged while every real-economy indicator collapsed.

The government rejected claims that India’s GDP is overstated by 22%, arguing that if that were true, official revisions would look very different. It said weaker links between GDP and traditional indicators are due to structural changes such as a larger services sector, lower manufacturing share, better GST compliance, and the 2019 corporate tax cut affecting direct tax data.

An important nuance is that earlier research also found GDP was underestimated during 2005–2011, suggesting the issue is less about political manipulation and more about flaws in methodology that distorted estimates in different periods.

Assessment: The decoupling is real and extensively documented. The government’s structural explanation is valid, but it explains part of the gap — not all of it. Both sides are partially right, which is precisely what makes this debate so hard to close.

Debate 2: Is the Informal Sector Being Measured Correctly?

The informal sector accounts for roughly 44% of GVA but employs approximately 90% of India’s workforce. Measuring it has always been hard.

The old methodology used corporate sector growth as a proxy for informal output — reasonable in the early 2000s, but structurally broken after demonetisation (2016), GST (2017), and COVID (2020–22), three shocks that hit the informal economy far harder than the formal one.

The most unsettling data point in the entire article is not a theoretical estimate — it is a government survey. Between 2015–16 and 2023–24, real earnings of informal sector workers grew at:

| Informal Sector | Annual Wage Growth (Real, 2015–2023) |

| Manufacturing | 2.7% |

| Trading | 1.7% |

| Other Services | 0.0% |

| All Informal | 1.3% |

Against a GDP growth story of 6%+ per year.

MoSPI’s counter is that formalisation is genuinely shifting output from the informal to the formal sector — so the informal sector’s shrinking share of GVA reflects reality, not mismeasurement. This is a defensible argument. But it creates a different, harder problem: if 90% of India’s workers are employed in a sector whose share of economic output is falling, the GDP growth story is structurally about a minority of the economy. The majority workforce is growing poorer relative to the headline.

There is also a pointed internal contradiction that the article surfaces: MoSPI noted that the 2017–18 Economic Survey — authored by Arvind Subramanian himself, then as Chief Economic Adviser — estimated that firms within the GST net accounted for nearly 80% of total turnover, implying a far more formalised economy than his 2026 paper assumes. The informal sector mismeasurement component accounts for 0.4–0.8 percentage points of the paper’s estimated overstatement. Subramanian’s 2026 paper makes no attempt to reconcile this.

Debate 3: WPI or CPI — Which Deflator Is Right?

To calculate real GDP — growth stripped of inflation — you need to “deflate” nominal output. India uses the Wholesale Price Index (WPI) as its primary deflator for manufacturing.

The researchers argue this has systematically inflated real GDP growth since 2014 for three reasons: WPI does not cover the services sector, it was dragged down by the collapse in global oil prices post-2014, and since 2011, WPI growth has averaged 2.2 percentage points below CPI growth — making the economy appear to grow faster in real terms than it actually did.

MoSPI defends WPI on the grounds that it aligns with producer-side valuation as recommended by the UN System of National Accounts, and that CPI — which includes retail margins, distribution costs, and taxes — is unsuitable for deflating production-side aggregates.

The new series partially concedes to critics by introducing double deflation and 500+ sector-specific price indices, but does not abandon WPI as the backbone. It is a genuine methodological improvement, but not the full switch to consumer prices the researchers wanted.

Who Is Affected — What GDP Revision Means for Real Stakeholders

| Stakeholder | Real Impact |

| Government & Finance Ministry | Fiscal deficit as % of smaller GDP now looks wider — fiscal consolidation narrative takes a hit |

| Foreign Investors & FPIs | India’s “size story” diminishes; potential sovereign rating pressure |

| IMF / World Bank Rankings | India slipped to 6th in IMF USD rankings following the revision |

| Welfare Policy Planners | Lower per-capita GDP means more citizens technically below poverty thresholds |

| Informal Sector Workers | 90% of the workforce whose 1.3% real wage growth the GDP headline never reflected |

| RBI & Monetary Policy | Growth projections used to calibrate repo rates — errors in GDP estimates transmit to monetary decisions |

| Bond Markets | Nominal GDP below 9% constrains revenue buoyancy and corporate profit growth |

The Deeper Problem the Article Underweights

The article is thorough on method and measured on politics. But it underweights what is the most structurally significant point: India is not running one economy — it is running two.

- The first is a formalising, GST-registered, digitally-enabled, corporate-driven economy growing at 7–8%.

- The second is an informal, unorganised economy employing nine out of ten Indian workers, growing real wages at 1.3% a year.

The GDP number — however accurately measured — captures the first economy far better than the second.

What to Watch: Four Markers That Will Define the GDP Credibility Story

1. The Back-Series Problem — The new series has usable data for only four years. A full historical back-series to 2011–12 is essential before the long-run growth narrative can be properly reassessed. MoSPI has signalled it is working on this, but it is not yet available.

2. The Informal Survey Cycle — The Survey of Unincorporated Enterprises is conducted every eight years. If this is not accelerated to an annual or biennial survey, 44% of GVA will continue to be estimated through proxies, and the methodology will remain vulnerable to the same criticism it faces now.

3. The IMF Cross-Check — The IMF revised India’s FY27 growth forecast to 6.4% in its April 2026 World Economic Outlook — against India’s official 7.6% for FY26. A persistent gap between IMF and official estimates is the clearest external signal that the credibility debate is not over.

4. The Rising Discrepancies — The new series has actually widened the discrepancy between production-side and expenditure-side GDP estimates. FY25 discrepancies rose 230% to ₹3.5 lakh crore, with FY26 projected at ₹4.9 lakh crore. If these gaps keep growing, they become the next major credibility flashpoint — regardless of how clean the methodology looks on paper.

India’s GDP number is not a fact — it is an estimate, built on surveys, proxies, deflators, and assumptions. The 2026 revision makes it a better estimate. Whether it makes it an honest one depends on how aggressively the informal sector, which employs nine out of ten Indian workers, is brought into the measurement frame — not just the formalisation narrative.

- Sign Up on Practicemock for Updated Current Affairs, Topic Tests and Mini Mocks

- Sign Up Here to Download Free Study Material

Free Mock Tests for the Upcoming Exams

- IBPS PO Free Mock Test

- RBI Grade B Free Mock Test

- IBPS SO Free Mock Test

- NABARD Grade A Free Mock Test

- SSC CGL Free Mock Test

- IBPS Clerk Free Mock Test

- IBPS RRB PO Free Mock Test

- IBPS RRB Clerk Free Mock Test

- RRB NTPC Free Mock Test

- SSC MTS Free Mock Test

- SSC Stenographer Free Mock Test

- GATE Mechanical Free Mock Test

- GATE Civil Free Mock Test

- RRB ALP Free Mock Test

- SSC CPO Free Mock Test

- AFCAT Free Mock Test

- SEBI Grade A Free Mock Test

- IFSCA Grade A Free Mock Test

- RRB JE Free Mock Test

- Free Banking Live Test

- Free SSC Live Test