India’s public land problem is staggering — 2.35 lakh acres lying idle with loss‑making CPSEs, plus millions more with Railways, Defence, and Ports. Procedural delays, valuation disputes, and overlapping claims have kept this resource locked for decades. With NMP 2.0’s ₹16.7‑lakh‑crore pipeline hinging on land monetisation, the Centre’s new framework finally defines “surplus land,” empowers NLMC as a single valuation authority, and sets the stage for unlocking value from dormant assets. In this Vishleshan, we decode why these rules matter for fiscal space, infrastructure speed, and India’s monetisation credibility in 2026–30.

Centre firms up new land-transfer norms to help public asset monetization

Context: The Department of Expenditure has issued consolidated guidelines governing the transfer and alienation of Central government land — replacing fragmented, decades-old ministry-level rules — to accelerate monetisation, redevelopment and transfer of public assets under NMP 2.0. This article unpacks what the framework does, why it was needed, and what the numbers actually mean once you look past the surface.

Link to the Article: Mint

India’s Public Land Problem — The Scale of What Has Been Sitting Idle

Government entities — railways, defence establishments, ports, state-run companies — hold vast tracts of land across India. The numbers are staggering:

- 2.35 lakh acres of surplus land identified with loss-making Central Public Sector Enterprises (CPSEs) alone

- CPSEs like MTNL, BSNL, Bharat Petroleum, BEML and HMT had identified approximately 3,400 acres for monetisation as per Economic Survey 2021-22 — this is a subset of the 2.35 lakh acre figure, not the same number

- Add Railways (India’s largest non-defence landowner), Defence establishments, and major Ports — the aggregate runs into millions of acres

Yet a substantial portion of this has remained unused or locked in low-value use because of:

- Procedural delays involving multiple committees across departments

- Ownership disputes with no nodal resolution body

- Overlapping claims between ministries with no clear hierarchy

- Complete absence of a uniform valuation mechanism — three departments could value the same plot at three entirely different numbers

NMP 2.0 is a ₹16.7 lakh crore pipeline. But if the land on which an infrastructure project must be built is stuck in paperwork between three ministries with three different valuation methods — the project doesn’t move. These guidelines are the traffic signal system for that pipeline.

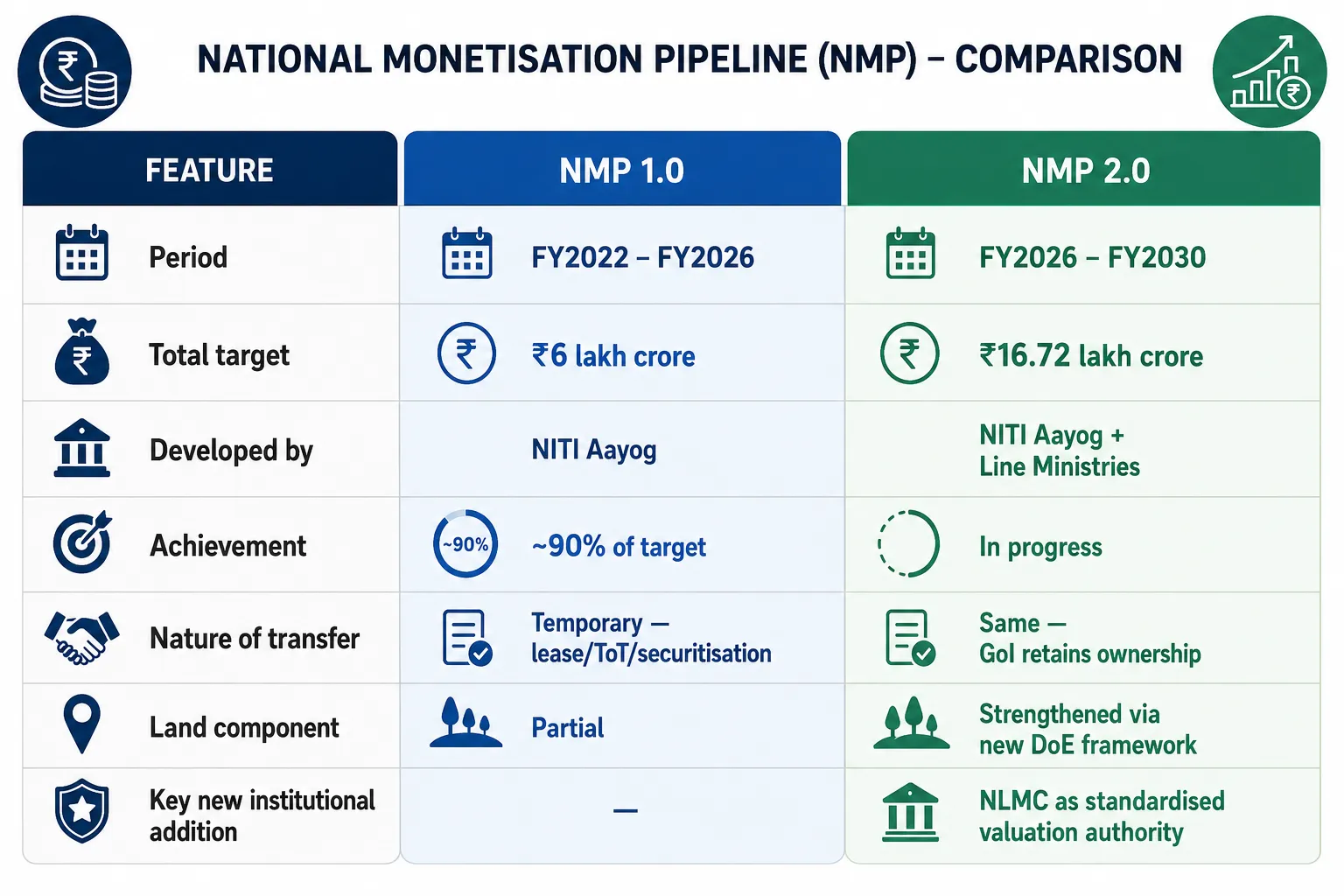

Background: What Is NMP 2.0?

The National Monetisation Pipeline (NMP) is India’s framework for unlocking value from existing government-owned infrastructure and assets by transferring their operational rights — not ownership — to private entities for a defined period.

NMP 1.0 (FY2022–FY2026) was developed by NITI Aayog in August 2021. It identified ₹6 lakh crore worth of Central government assets across sectors — roads (ToT), railways, power transmission, gas pipelines, telecom towers, airports, ports, warehousing, and mining — to be monetised over four years. NMP 1.0 achieved approximately 90% of its target — a creditable outcome for a first-of-its-kind exercise.

NMP 2.0 (FY2026–FY2030) was announced in Union Budget 2025-26. At ₹16.72 lakh crore, it is 2.79 times the size of NMP 1.0. It was developed by NITI Aayog in consultation with line ministries and includes a significantly expanded role for land monetisation — which NMP 1.0 had touched only partially. The private sector is expected to contribute ₹5.8 lakh crore of the total.

The critical conceptual point: Asset monetisation is not the sale of government assets. Under NMP, the government transfers the right to operate and earn revenues from an asset — through mechanisms like:

- ToT (Toll-Operate-Transfer): Private player collects tolls/revenues for a defined concession period

- Long-term leases: Asset leased to private operator for 30–99 years

- Securitisation of cash flows: Future revenue streams from an asset are securitised and sold to investors

The government retains ownership throughout. At the end of the concession, the asset reverts. This distinction matters enormously — and is the most commonly misrepresented fact about NMP in public discourse.

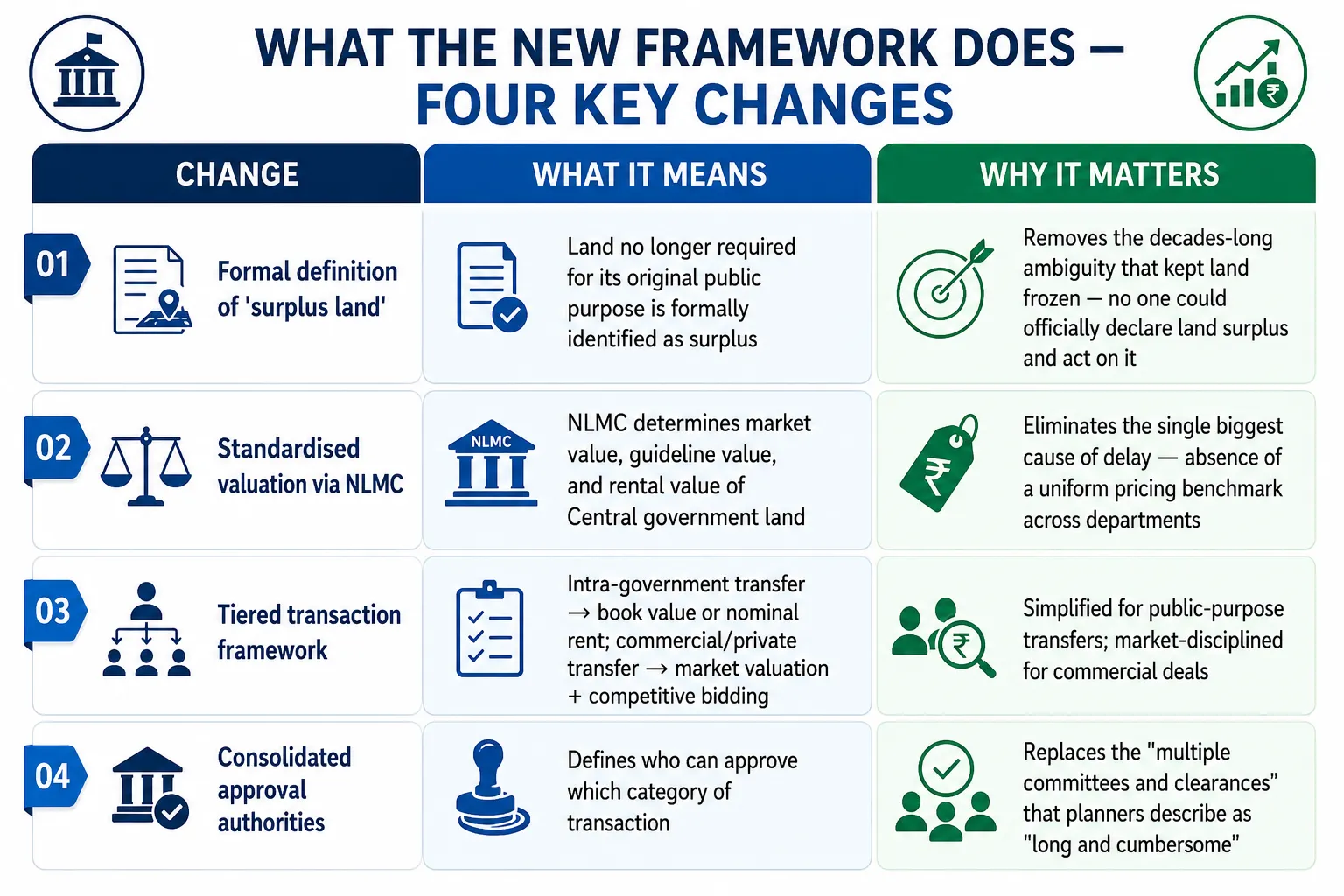

What the New Framework Does — Four Key Changes

Decoding the article: Analysis

1. ‘Surplus Land’ Was Never Formally Defined Before. That Is the Real Story.

- Until this framework, there was no administrative definition of “surplus land” in Central government rules. Land acquired in 1968 for a factory that shut in 1995 — no department could officially declare the remaining land surplus and move it. It sat in legal limbo: not used, not transferable, not leaseable, generating zero value for decades.

- The new framework defines surplus land as land no longer required for the original public purpose for which it was acquired. Those original purposes include: Setting up of offices, housing, railways, factories, hospitals, schools, and other public infrastructure

- Once declared surplus, the land can be transferred between government entities (book value), leased for infrastructure/utility projects (market value), or commercially monetised via competitive bidding (market value). The act of formal identification — bureaucratically simple-sounding — is what unlocks everything downstream. Without that first step, no valuation body, no bidding process, and no framework can function.

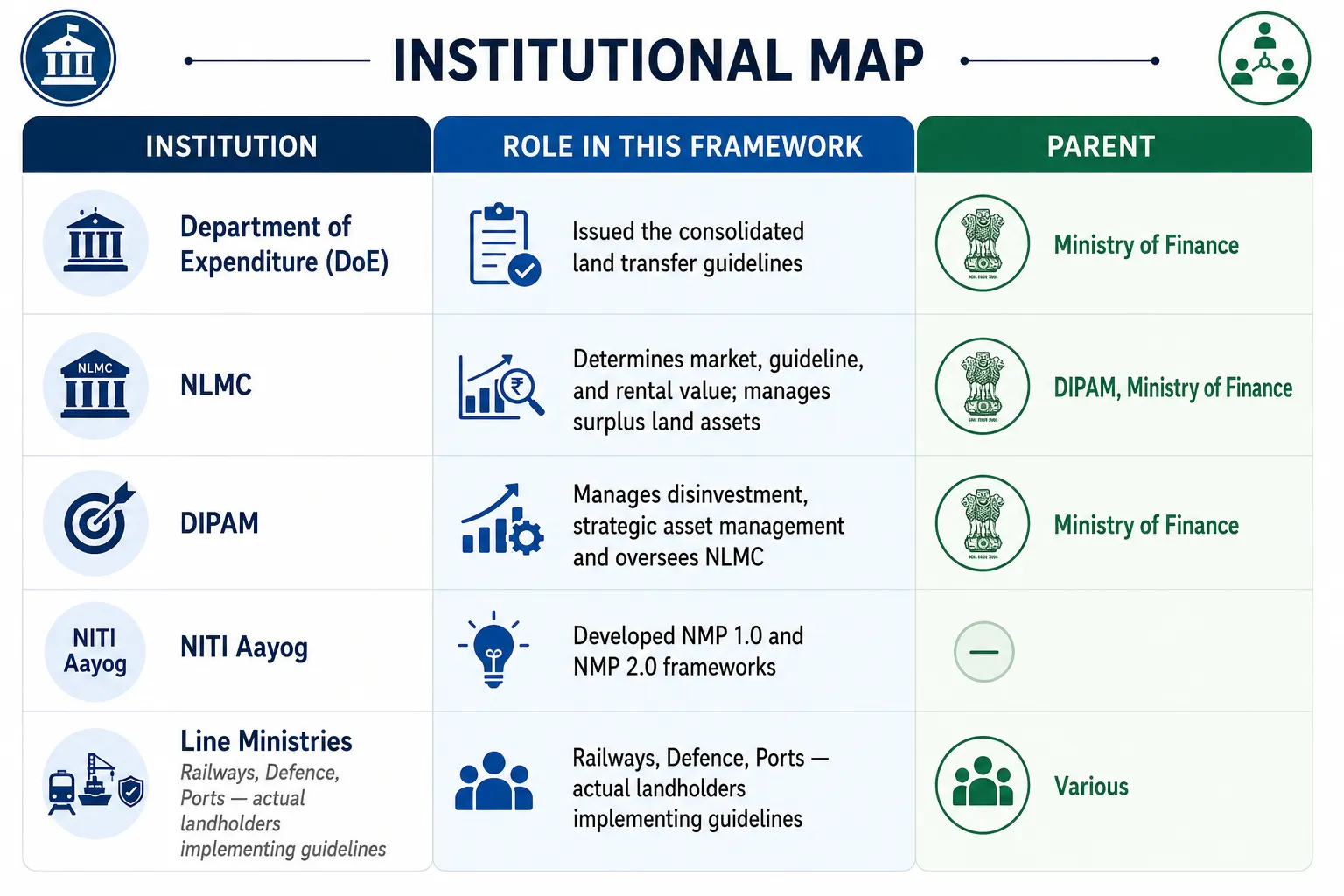

2. NLMC’s Role Is More Significant Than the Article Suggests

- The article mentions NLMC (National Land Monetisation Corporation) almost in passing — as a “valuation body.” That undersells what is happening institutionally.

- NLMC was set up in August 2022 as a 100% Government of India company under the Companies Act, under DIPAM (Department of Investment and Public Asset Management), Ministry of Finance. Its original mandate: monetise surplus, non-core land and assets of CPSEs.

- What this framework does is expand and operationalise NLMC’s role — it becomes the de facto land bank manager for all Central government land, not just CPSE assets. By empowering NLMC to determine three distinct types of value — market value, guideline value, and rental value — the government has created a single pricing authority that removes the departmental turf wars over who values what and how.

- The institutional relationship worth knowing cold: DIPAM handles privatisation and strategic disinvestment of CPSEs. NLMC handles their non-core asset monetisation. They are complementary, not overlapping — one disposes of the enterprise, the other unlocks the real estate.

3. The Framework Cannot Solve the State-Level Land-Use Conversion Problem

- V. P. Kulshrestha’s quote is carefully worded: “In many cases, changes in land-use approvals are also required, particularly where some development or improvement has already taken place.”

- This is the unresolved federal friction the framework cannot fix on its own.

- The constitutional reality: land is Entry 18 of List II (State List) of the Seventh Schedule — states have primary legislative authority over land-use regulation. A change of land-use — converting old MTNL exchange land from “telecommunication use” to “commercial real estate,” for instance — requires state government approval under applicable Town and Country Planning Acts.

- The Centre can identify the land as surplus. NLMC can value it. The DoE framework can authorise the transaction. But if the state government sits on the land-use conversion application for two years, the entire process stalls — and the ₹2.35 lakh acre potential stays locked in a different kind of bureaucratic limbo.

- This means every major commercial monetisation of Central government land in urban areas will still depend on state government cooperation — a federal variable that the DoE guidelines, however well-designed, cannot control.

The Fine Print — What the Article Does Not Say Loudly Enough

- The 3,400 acres and 2.35 lakh acres are two different numbers referring to two different things. 3,400 acres is from Economic Survey 2021-22 and refers specifically to five named CPSEs. 2.35 lakh acres is the aggregate for all loss-making CPSEs.

- ₹16.72 lakh crore is a pipeline aspiration, not a committed disbursement. NMP 1.0 achieved ~90% of target — impressive, but not complete. NMP 2.0 at 2.79× the scale relies on significantly more moving parts: more sectors, more states, more private capital, and now a much more ambitious land component that has never been tested at this scale with a unified framework.

- Amit Singh (JNU) notes the framework will “facilitate redevelopment of old government colonies.” This is the least-discussed but potentially most transformative application — old GPRA (General Pool Residential Accommodations) colonies in prime urban land in Delhi, Mumbai, Bengaluru, Chennai represent some of the highest-value land parcels in the country. Their monetisation would dwarf the value of remote industrial land. The article gestures at this but does not develop it.

- The framework covers UTs without legislature — not all UTs. UTs with legislature (Delhi, Puducherry, Jammu & Kashmir) have their own assemblies and some legislative autonomy. The distinction matters for implementation because land-use approvals in those UTs follow a different political and administrative path.

Institutional Map

What to Watch

NLMC’s first standardised valuation circulars (Q2 FY27) — the real-time test of intent: when NLMC publishes its first benchmarks for land categories across major cities and states, the market will immediately scrutinise whether the “standardisation” is genuinely market-reflective or conservatively understated to avoid political friction. Undervaluation defeats the fiscal purpose; overvaluation kills commercial interest. The first set of NLMC circle-rate comparisons will be the proof of concept for this entire framework.

The first major commercial land transaction under the new rules (FY27) — the lagging confirmation: the framework is new as of May 2026. The first large-ticket transaction — surplus MTNL land in Delhi, a railway goods shed in Mumbai, a BEML industrial plot in Bengaluru — will set the precedent for competitive bidding processes, state-level land-use approvals, and actual revenue generation timelines. If the first transaction takes 18 months and 11 committees despite the framework, it signals that the procedural culture has not changed even if the rules have.

State government response to land-use conversion requests — the structural friction driver: states that cooperate quickly — particularly the large commercial real estate markets of Maharashtra, Karnataka, Delhi NCR and Tamil Nadu — will determine how much of the ₹2.35 lakh acre potential actually converts into monetised value within the NMP 2.0 timeframe. Watch for formal state-Centre MoUs on fast-track land-use approvals as the leading indicator that federal friction is being actively managed rather than hoped away.

In 1991, India pledged its gold reserves to keep the lights on. In 2021, it mapped its assets and said: let the private sector run them, we keep the title. In 2026, it is doing something more fundamental — it is finally deciding that the land beneath those assets is itself a resource, and that leaving 2.35 lakh acres of it idle while borrowing money for infrastructure is a choice India can no longer afford to make.

- Sign Up on Practicemock for Updated Current Affairs, Topic Tests and Mini Mocks

- Sign Up Here to Download Free Study Material

Free Mock Tests for the Upcoming Exams

- IBPS PO Free Mock Test

- RBI Grade B Free Mock Test

- IBPS SO Free Mock Test

- NABARD Grade A Free Mock Test

- SSC CGL Free Mock Test

- IBPS Clerk Free Mock Test

- IBPS RRB PO Free Mock Test

- IBPS RRB Clerk Free Mock Test

- RRB NTPC Free Mock Test

- SSC MTS Free Mock Test

- SSC Stenographer Free Mock Test

- GATE Mechanical Free Mock Test

- GATE Civil Free Mock Test

- RRB ALP Free Mock Test

- SSC CPO Free Mock Test

- AFCAT Free Mock Test

- SEBI Grade A Free Mock Test

- IFSCA Grade A Free Mock Test

- RRB JE Free Mock Test

- Free Banking Live Test

- Free SSC Live Test