For India’s policymakers, NITI Aayog’s projection that Digital Public Infrastructure (DPI) could contribute 4% of GDP by 2030 is more than a headline statistic. It signals a shift from DPI as a tool of inclusion to DPI as an engine of productivity. What looks like a technical forecast is in fact a structural wager: can India’s open‑source digital stack evolve from Aadhaar and UPI into a growth driver on par with physical infrastructure? The deeper story is whether DPI 2.0 can overcome data silos, cybersecurity risks, and literacy gaps to unlock exponential gains, or whether these unresolved bottlenecks will stall the 4% thesis. In this Vishleshan, we decode NITI Aayog’s argument, track the layers of DPI, and assess if India’s digital backbone can truly become its next growth multiplier.

Digital public infrastructure could account for 4% of GDP by 2030: NITI Aayog

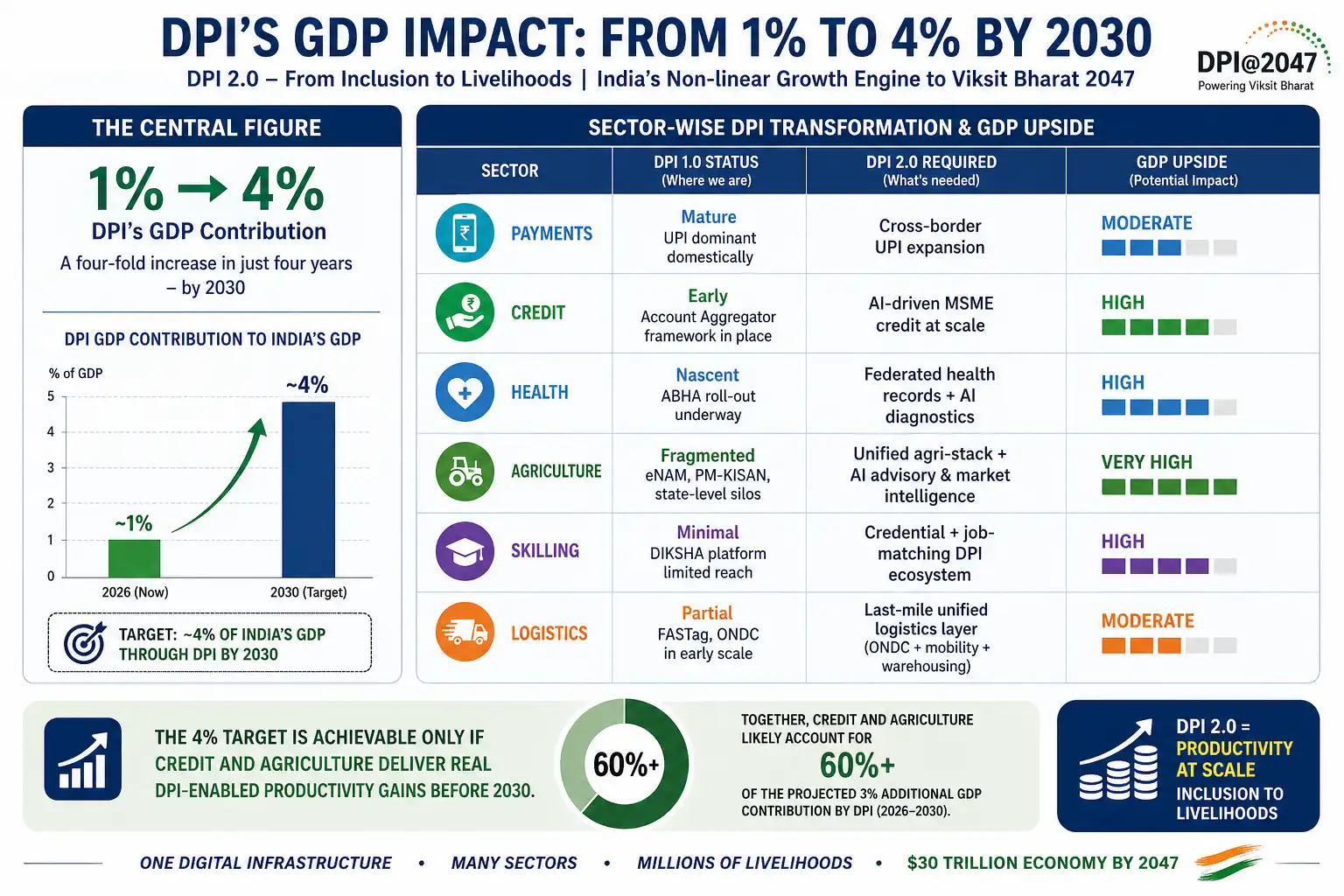

Context: On April 27, 2026, NITI Aayog released its DPI@2047 strategic roadmap — arguing that India’s digital public infrastructure, currently contributing 1% of GDP, could rise to 4% by 2030 if the next phase is executed well. DPI 1.0 brought India online, while DPI 2.0 must turn that digital access into real gains in jobs, credit, health, and productivity for the 800 million lower- and middle-income Indians still outside the full reach of the formal economy. This article covers what DPI 1.0 built, what DPI 2.0 must deliver, where AI fits in, and what the honest constraints are on getting from 1% to 4%.

Link to the Article: Mint

What Is Digital Public Infrastructure?

- Digital Public Infrastructure is the shared digital foundation that both government and private businesses run on. It is open, interoperable, and built for population scale — think of it like roads and electricity grids, except digital. Nobody owns it exclusively, but the entire economy depends on it.

- India began building this foundation in 2009 with Aadhaar and kept adding layers through UPI (2016), GST (2017), FASTag (2017), and beyond. The architecture sits on the JAM Trinity — Jan Dhan accounts, Aadhaar, and Mobile connectivity — which together form the backbone of India’s digital financial system. It is governed by MeitY, with NITI Aayog’s Frontier Tech Hub coordinating its next phase.

- The reason DPI exists is simple: formal markets, banks, and government services historically bypassed hundreds of millions of Indians. DPI was built to solve that last-mile problem at scale — and by most measures, it has. The DBT system built on DPI is today the world’s largest government-to-person payment infrastructure.

- DPI 1.0 focused on access and inclusion. DPI 2.0 is about turning that access into economic productivity and livelihoods.

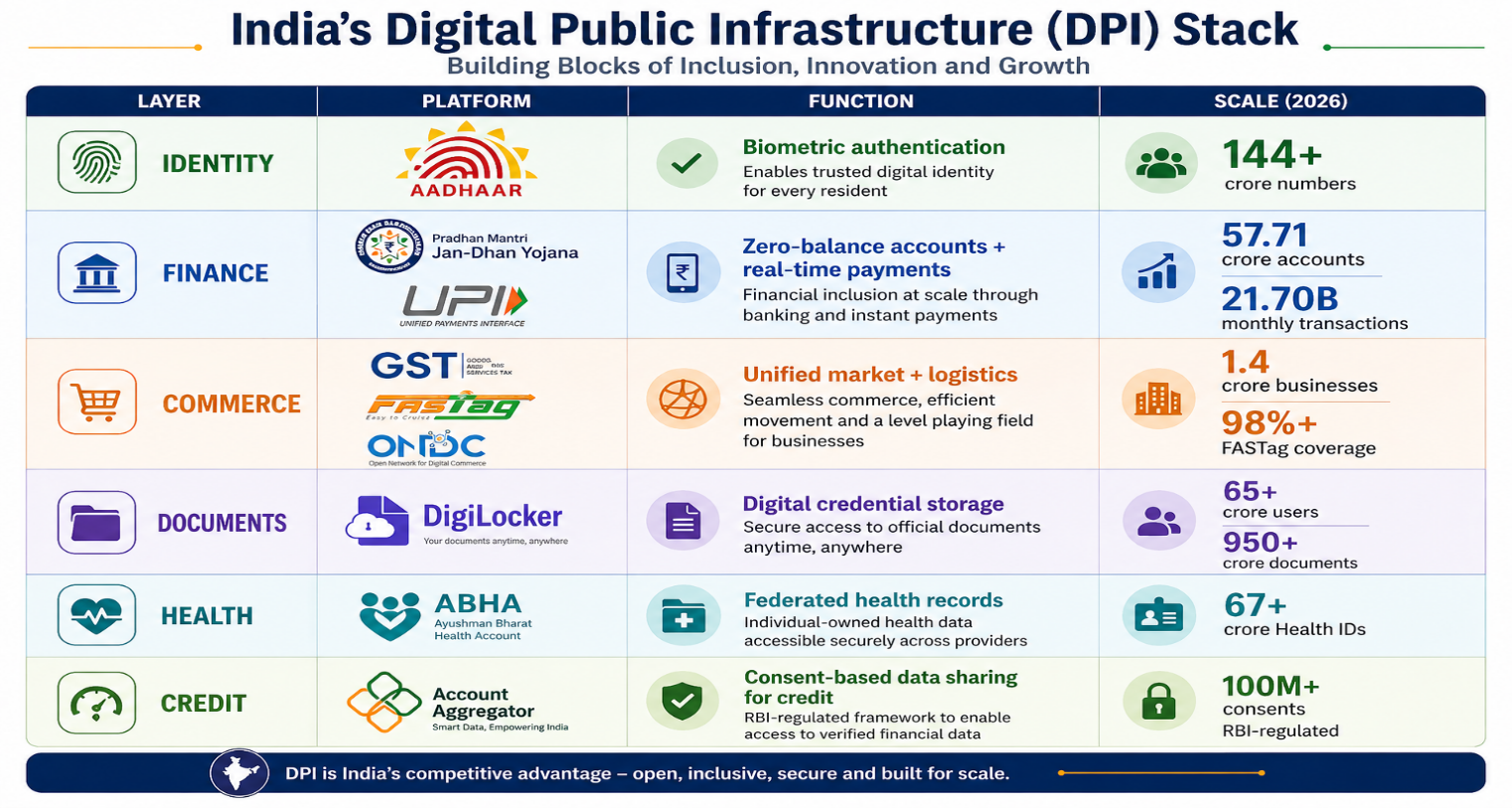

What DPI Actually Controls — The Six Layers

DPI is not one platform. It is a stack of interlocking layers, each enabling the one above it:

When these layers work together, DPI creates non-linear growth — each new user makes the system more valuable for every existing user. That network effect is exactly what NITI Aayog means when it says DPI’s growth trajectory is “exponential, not linear“.

Three Layers Beyond the Headline

Layer 1 — What DPI 1.0 Built: Access at Scale

- DPI 1.0 was structural. It pulled hundreds of millions of excluded citizens into the formal economy in under a decade. Jan Dhan opened 57.71 crore bank accounts. Aadhaar gave 144 crore residents a verifiable identity.

- UPI processed 21.70 billion transactions in a single month. DBT transferred ₹7.5 lakh crore directly to citizens, cutting welfare leakages from 30-40% to under 10% in key schemes.

- GST brought 1.4 crore businesses onto a single digital tax platform. This was not an improvement on the old system. DPI 1.0 replaced it.

Layer 2 — What DPI 2.0 Must Do: Productivity, Not Just Access

- India now has 800 million people who are digitally included — Aadhaar, Jan Dhan, UPI — but not economically productive within the formal system. They have bank accounts but no credit history. GST numbers but no working capital. They are formally employed but outside any skilling or social protection system.

- DPI 2.0’s job is to convert that inclusion into productivity — using AI, open credit networks, health platforms, and logistics infrastructure to make the formal economy actually work for the people who are technically inside it. Getting people into the system was DPI 1.0’s job. Making the system work for them is DPI 2.0’s.

Layer 3 — AI Is the Multiplier — But Data Silos Are the Wall

- The report’s most ambitious argument is that AI integrated into DPI creates exponential gains.

- An Aadhaar-authenticated farmer receiving an AI soil advisory. A Jan Dhan holder getting an AI-assessed micro-credit offer in 30 seconds. A GSTN-registered MSME accessing AI-generated export guidance for its specific product. Every one of these is technically possible today.

- What blocks them is not technology — it is data silos. Aadhaar, GSTN, ABHA, DigiLocker, and the Account Aggregator do not share data by default.

- Each needs separate consent, separate authentication, and separate integration. Until a unified consent and data-sharing layer is built, AI cannot access the cross-platform data it needs. The report calls AI DPI’s multiplier. What it doesn’t say loudly enough is that data fragmentation is the wall AI cannot climb alone.

The Big Number: 1% → 4%

DPI’s GDP contribution rising from 1% to 4% by 2030 — a four-fold increase in four years — is the central figure the report builds around:

Action Agenda: Four Reforms DPI 2.0 Needs Now

| # | Area | The Problem | What Needs to Be Done | Why It Matters |

| 1 | Data Interoperability | Aadhaar, GSTN, ABHA, DigiLocker, and Account Aggregator don’t interact to each other by default. Every cross-platform service needs separate consent, separate authentication, and separate API integration — blocking AI from generating real value | Build a unified consent and data-sharing layer (DEPA model) covering all DPI platforms under one citizen-facing dashboard. Mandate open, standardised APIs across the entire DPI stack | AI’s multiplier effect only works if data flows freely with citizen consent. Without this layer, the 1% → 4% GDP target stays a projection, not a reality. |

| 2 | DPDP Rules | The DPDP Act was passed in 2023; implementing rules notified November 2025 with an 18-month compliance window (deadline: May 2027). Every AI-powered DPI application — credit, health, agriculture — operates in a legal grey zone until then. | Issue AI-specific consent guidelines under the DPDP Rules immediately for DPI-linked applications. Mandate verifiable, purpose-tagged, multilingual consent for all citizen-facing DPI services. | When an AI system makes a harmful decision using a citizen’s DPI data, there must be a statutory remedy. Operating without this framework is building on a legal foundation that does not yet exist. |

| 3 | Cybersecurity | DPI’s open-source stack (Linux, OpenBSD) is vulnerable to AI-discovered zero-days — as the Mythos report (April 2026) flagged. A single compromised DPI layer does not affect one company — it affects every citizen and every service built on it | Mandate AI-assisted vulnerability scanning for all DPI code before every major deployment. Establish a DPI Cybersecurity Response Cell under CERT-In. Adopt a zero-trust architecture across all inter-platform DPI communications | Scaling DPI without scaling its security is building a larger and more systemically dangerous target. A breach on UPI or Aadhaar is not a data incident — it is a national economic security event. |

| 4 | Digital Literacy | UPI is near-universal in cities. But DPI 2.0’s target — 800 million lower- and middle-income Indians — is largely rural, with inconsistent smartphone access, internet reliability, and digital skills. Sophisticated AI services are useless if the citizen cannot navigate them. | Fund targeted digital literacy missions in PLFS-identified low-participation districts. Deploy assisted-access models — CSCs, local operators, and voice-based vernacular interfaces — as parallel channels for AI-powered DPI services. | The highest DPI 2.0 GDP upside — credit and agriculture — depends entirely on rural citizens being able to access and trust these services. Literacy is not a soft concern. It is a hard prerequisite for the headline number. |

What to Watch

The immediate priority is Account Aggregator MSME credit penetration. If AI-powered credit disbursals through the AA network scale to 50 lakh MSMEs by March 2027, the 4% GDP thesis gets its first credible proof point — moving DPI 2.0 from a policy document to a measurable economic reality. Simultaneously, the DPDP Rules compliance timeline is the single most important regulatory signal to watch. Every month of delay blocks the consent and data-sharing layer that DPI 2.0’s entire AI integration depends on.

Three indicators to track over the next two quarters:

| Indicator | What to Watch | Why It Matters |

| AA-based MSME Credit | Does disbursement cross ₹1 lakh crore by Q3 FY27? | First hard proof point for the 4% GDP thesis |

| DPDP Rules | Are AI-specific consent provisions operational before August 2026? | August 2026 is also the EU AI Act enforcement deadline — Indian startups with EU exposure face dual pressure |

| DPI Cybersecurity | Does any DPI system suffer a Mythos-class breach in FY27? | A breach on UPI or Aadhaar is not a data incident — it is a national economic security event |

If all three move in the wrong direction simultaneously — credit stagnates, DPDP Rules stay delayed, and a major breach occurs — the conversation will shift from “DPI 2.0 is India’s growth engine” to “DPI 2.0 is India’s biggest unmanaged systemic risk.”

- Sign Up on Practicemock for Updated Current Affairs, Topic Tests and Mini Mocks

- Sign Up Here to Download Free Study Material

Free Mock Tests for the Upcoming Exams

- IBPS PO Free Mock Test

- RBI Grade B Free Mock Test

- IBPS SO Free Mock Test

- NABARD Grade A Free Mock Test

- SSC CGL Free Mock Test

- IBPS Clerk Free Mock Test

- IBPS RRB PO Free Mock Test

- IBPS RRB Clerk Free Mock Test

- RRB NTPC Free Mock Test

- SSC MTS Free Mock Test

- SSC Stenographer Free Mock Test

- GATE Mechanical Free Mock Test

- GATE Civil Free Mock Test

- RRB ALP Free Mock Test

- SSC CPO Free Mock Test

- AFCAT Free Mock Test

- SEBI Grade A Free Mock Test

- IFSCA Grade A Free Mock Test

- RRB JE Free Mock Test

- Free Banking Live Test

- Free SSC Live Test